In times of market decline, it’s easy to fall into the trap of reacting impulsively. However, it’s important to remember that successful investing is about playing the long game not making knee-jerk reactions to short-term market fluctuations. By staying committed to a long-term strategy, you’re more likely to achieve your financial goals, rather than chasing quick profits that are often elusive.

The secret to long-term success lies in sticking to a well-thought-out strategy, which is far more effective than chasing short-term profits that often lead to disappointment. Let’s explore why maintaining a long-term approach is crucial for achieving your financial objectives.

When markets fall, it’s natural to feel the urge to “do something.” Whether it’s selling off assets or trying to time the market. The idea of quick profits and instant gratification can be very appealing, especially when you see a sudden dip in prices. Some investors may attempt to buy and sell based on predictions of short-term market movements, believing they can beat the market by making the right moves at the right times.

However, market timing, which involves buying and selling based on predictions of market direction, is often a strategy fraught with risk. Numerous studies show that this approach tends to yield suboptimal results in the long run, as accurately predicting the market is nearly impossible.

The core of market timing revolves around predicting price movements and making decisions based on those predictions, whether to buy when you think prices will rise or sell when you anticipate a decline. The goal is to capitalise on these forecasts to generate short-term profits. However, the challenge lies in the unpredictable nature of the market.

Markets are influenced by a wide range of factors, from economic indicators to geopolitical events, making it incredibly difficult to predict short-term movements. For those trying to time the market, two correct decisions are needed: when to exit and when to re-enter. Getting either of these wrong can lead to significant financial losses. And remember, even the most experienced investors can’t consistently predict market movements.

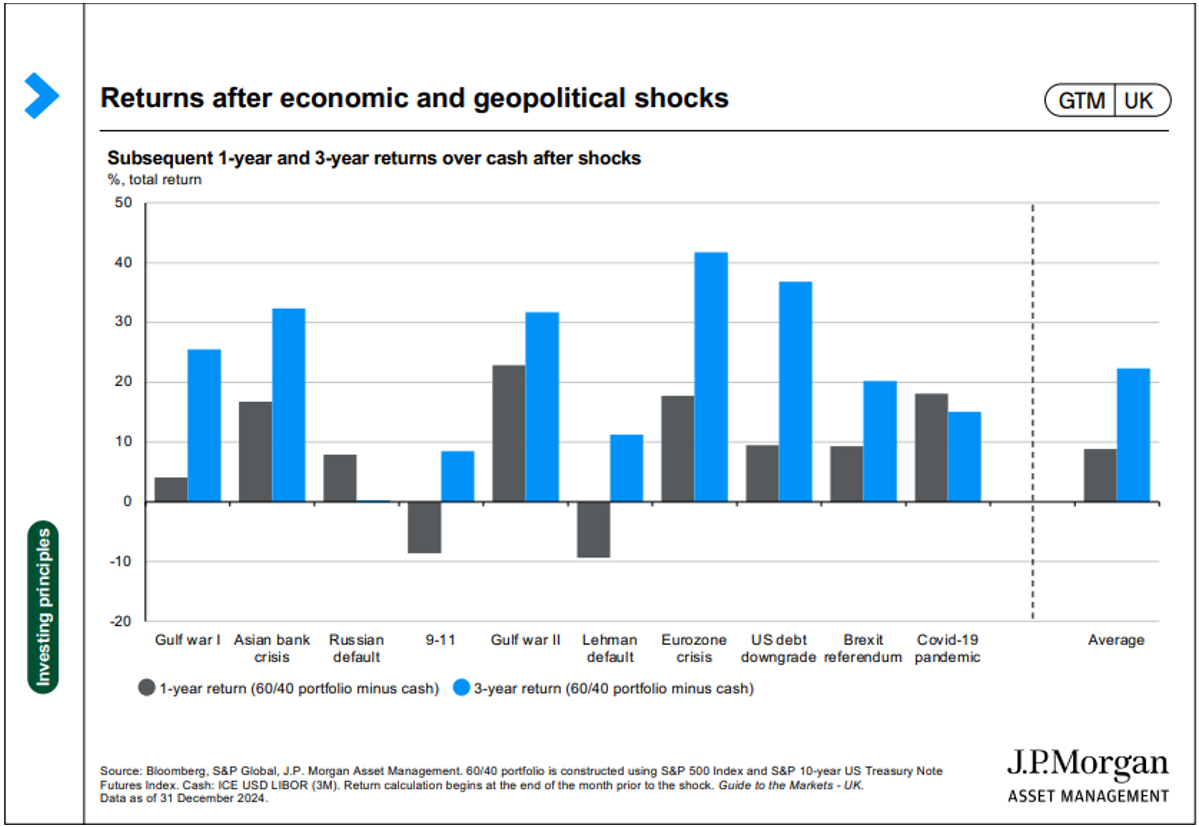

For example, sheltering in cash can be tempting after economic and geopolitical shocks but history suggests this is rarely a good idea. When looking at a select number of shocks since 1990, a 60/40 portfolio of stocks and bonds has outperformed cash 80% of the time over a 1-year horizon, and always over a three-year timeframe:

Instead of trying to time the market, focus on strategies that embrace long-term growth and consistent investing. One of the most effective methods is pound cost averaging, which involves investing a fixed amount regularly, regardless of market conditions. This strategy smooths out the volatility by investing consistently over time, rather than attempting to catch the “perfect” moment.

For example, instead of investing a lump sum all at once, you might decide to invest a fixed amount each month, say £1,000. This reduces the risk of buying during an inflated market and allows you to benefit from purchasing more shares when prices are lower. It’s an approach that minimises the emotional side of investing especially during market downturns.

While it’s tempting to react to market dips, the key to long-term investing success is consistency. Pound cost averaging enables you to weather short-term market fluctuations by focusing on regular contributions over time, instead of worrying about when to buy or sell. Over the long term, this approach allows you to accumulate more assets at lower prices during market downturns.

And while this method doesn’t guarantee a profit, it does tend to mitigate the risk of emotional decisions and knee-jerk reactions. By focusing on time in the market, you let the power of compound growth and consistent investment work for you.

In conclusion, when the market dips, remember that your best option is often to stay steady and let your investments grow over time. Stick with your plan, resist the urge to act impulsively, and enjoy the benefits of consistent, patient investing.

If you’re looking to revisit your financial plan or explore new investment opportunities, we’re here to guide you. Our team can offer personalised advice and insights tailored to your unique circumstances, helping you navigate uncertainty with confidence.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

If you want to build a solid, robust investment portfolio that can withstand market volatility and deliver long-term growth, diversification is a must in building a strong, resilient investment portfolio. Diversification is a key strategy to protect your investments from market volatility and set yourself up for long-term growth.

The secret to achieving lasting success lies in balancing risk and opportunity through a well-diversified approach. Let’s dive into why diversification is essential for your financial future and how you can implement it effectively in your investment strategy.

Diversification involves spreading your investments across various asset classes, industries, and geographical regions. This approach helps reduce risk by ensuring that no single downturn will severely impact your entire portfolio. The core idea is simple: don’t put all your eggs in one basket.

For example, if you only invest in one stock or asset class, like equities, any negative market movement could have a major impact on your wealth. However, by diversifying into multiple asset type such as stocks, bonds, real estate, and commodities, you create a more resilient portfolio. Different assets often perform differently during market changes, ensuring your overall financial health is better protected.

In today’s volatile investment climate, diversification acts as a buffer against unpredictable market shifts. Economic events, government policy changes, or fluctuations in interest rates can all cause specific sectors or asset classes to perform poorly. But a diversified portfolio spreads these risks across various areas.

For instance, when stock markets experience downturns, bonds can provide a stabilising effect. Likewise, investing in international markets or alternative assets like gold can provide a cushion when other parts of your portfolio are underperforming. By spreading your investments, you can weather storms more effectively and minimise the chance of significant financial loss.

While risk management is one of the primary advantages, diversification also plays a pivotal role in maximising long-term returns. By gaining exposure to different asset classes, you increase the likelihood of capturing growth opportunities across sectors.

Consider the following: equities might offer high growth potential but come with more risk, while bonds are less volatile and provide stability. A balanced mix of both allows you to manage risk while still positioning yourself for potential growth. Additionally, as different industries thrive at different times, your diversified portfolio enables you to capitalise on opportunities across the economy. A diversified approach ensures you’re positioned to benefit from multiple sectors’ successes.

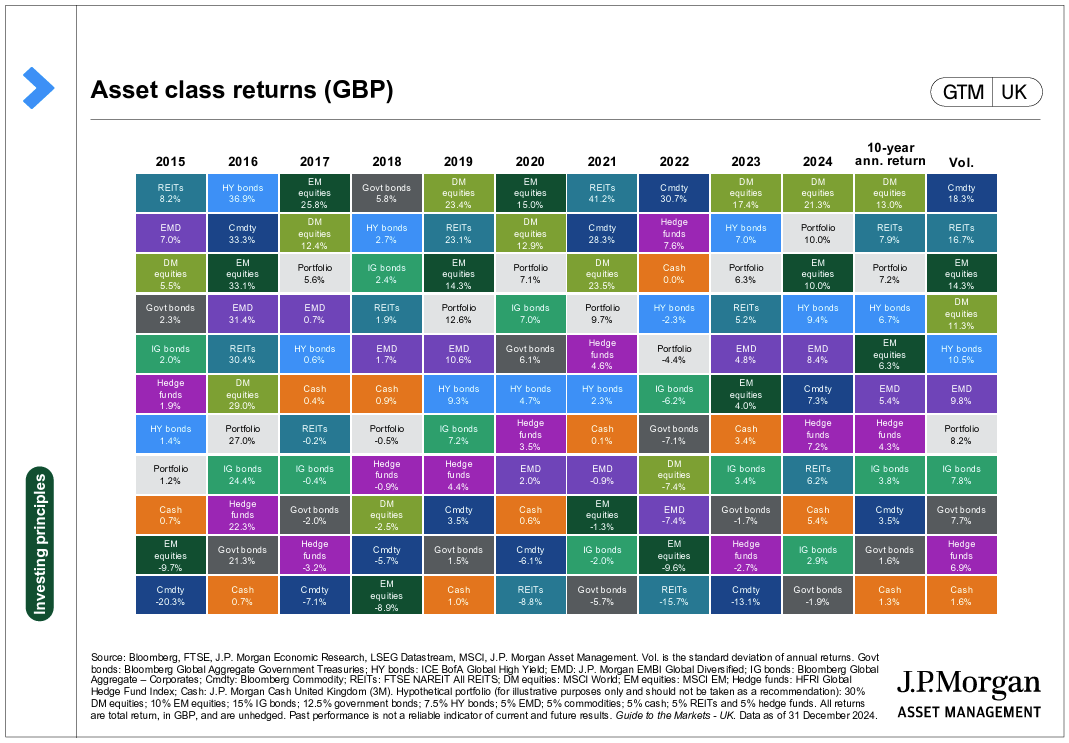

The proverbial ‘patchwork quilt’ chart below neatly illustrates the importance of diversification. It shows the returns of various assets classes and that of a representative diversified portfolio over the last 10 years, with the penultimate column being their respective annualised 10-year returns.

There is huge variation in winners and losers in any discrete year, but interestingly the well-diversified portfolio, including stocks, bonds and some other asset classes, has returned around 7% per year over this time period. While the risk of loss is still an unavoidable part of investing, the diversified portfolio has also provided a much smoother ride for investors than investing in equities alone, as shown by its position in the chart’s volatility column

A diversified investment strategy must be tailored to each individual’s financial goals, time horizon, and risk tolerance. Every investor’s situation is different. What works for one person may not work for another. Some may prefer a more aggressive investment strategy with a focus on equities, while others might want greater stability with more bonds or cash.

Regular portfolio reviews and adjustments are crucial for staying on track toward your financial goals. Major life events, such as changes in income, family obligations, or retirement plans, may require modifications to your portfolio’s allocation. This is where professional advice becomes invaluable.

So, the key things to remember are :

Diversification isn’t just a buzzword; it’s a critical strategy for managing risk and achieving financial success over the long term. By diversifying your investments across various asset classes, sectors, and geographical regions, you create a more resilient portfolio while increasing the likelihood of growth.

If you’re unsure whether your portfolio is well-diversified, or if you need guidance on creating a strategy that aligns with your financial goals, don’t hesitate to reach out for professional advice. As your trusted independent financial adviser, Fairstone is here to help you create a portfolio that can stand the test of time and help you reach your financial aspirations.

Remember, the secret to successful investing is not just about identifying the right opportunities it’s about ensuring that your portfolio is strategically designed to navigate the inevitable ups and downs of the market. Diversification is the proven strategy that can help you do just that!

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

The purpose of this blog is to provide you with clarity amid the recent turbulence in global markets, triggered by the US administration’s actions. These market shifts affect not only businesses and trade but also have a direct impact on your personal financial landscape, from pensions to mortgages, inflation to taxes. The secret to navigating this uncertainty and emerging stronger lies in maintaining a long-term perspective. Rather than reacting impulsively, it’s about sticking to a strategy grounded in diversification, smart planning, and patience. Let’s explore what’s happening and how you can position yourself for long-term success.

There’s no sugar-coating, global markets took a hit in response to the tariffs. But if you’re investing for the long term, market volatility isn’t something to fear, it’s something to expect.

That’s why the timeless investing principles of time in the market and diversification matter more than ever.

Trying to time the market, buying low and selling high with perfect precision, is extremely difficult, even for professionals. Instead, history shows that staying invested through market ups and downs gives you a much better chance of long-term success. Missing just a few of the market’s best days can significantly reduce returns.

Just as important is diversification. Spreading your investments across regions, industries, and asset types helps cushion your portfolio against shocks in any one area. It’s your best defence against the unexpected and trade tariffs certainly count as that.

For pension investors, the recent volatility may feel unsettling. But reacting impulsively by cutting contributions or changing strategy could lock in losses and harm your future retirement income.

If you’re nearing retirement, it might be wise to delay taking income via drawdown until markets stabilise. Alternatively, more people may consider annuities, especially while rates remain attractive. Right now, a 65-year-old with a £100,000 pension could secure up to £7,685 a year from a level annuity with a five-year guarantee.

Just remember annuities are usually fixed for life, so it’s crucial to weigh all options before committing.

If you’re already in retirement using drawdown, consider a natural yield approach—only withdrawing income generated by your investments. And to weather short-term storms, hold one to three years’ worth of essential expenses in an easy-access account.

It’s tough to predict how tariffs will ultimately affect inflation. On one hand, companies may raise prices to offset higher costs. On the other, we might see price wars as firms compete for access to the US market or UK consumers could benefit from surplus goods diverted from the US.

This inflation uncertainty complicates things for the Bank of England. For now, markets expect further interest rate cuts to support economic growth, which could be good news for borrowers.

What about mortgages? If you’re due to remortgage, it’s worth locking in a deal early. Rates may fall further but if they rise, you’ll be glad you secured a lower rate now.

Could taxes go up? If growth slows due to global uncertainty, the government may be forced to find ways to raise revenue especially come Autumn Budget season. That’s why now is a great time to take advantage of existing tax wrappers like ISAs and pensions, which can help protect more of your money from future tax changes.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

In a recent move that has heightened global trade tensions, the US administration announced a series of sweeping reciprocal tariffs. In response, China has introduced a 34% blanket tariff on all US imports starting April 10, alongside export restrictions on critical rare earth materials and sanctions targeting key US defence and technology firms.

The purpose of this blog is to help you navigate the recent surge in global trade tensions and understand the long-term impact of these events on your financial strategy. These trade moves could have a ripple effect on markets, impacting everything from stock prices to supply chains, but the key to weathering this uncertainty lies in staying focused on your long-term goals. Remember, the secret to long-term success in investing isn’t about trying to time the market, it’s about time in the market. Despite the noise, sticking to a consistent strategy is what will ultimately drive your success.

Markets can, and do, experience periods of downturns. These moments may feel unsettling, but they’re typically short-lived. The most effective approach is to stay committed to your investment strategy, even when markets are turbulent.

History has consistently shown that drawdowns are entirely normal in any given year, and that markets recover and often bounce back just as sharply as they fall. Trying to time the market by selling in a panic or holding off on new investments until things “settle down” can significantly impact your long-term financial returns.

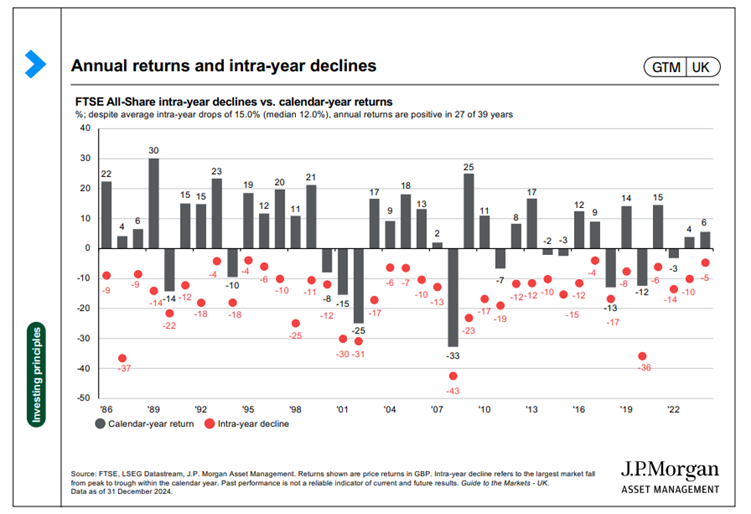

In the chart below looking at the UK FTSE All-Share index over a near-40 year period, the red dots represent the maximum intra-year equity decline in every calendar year, or the difference between the highest and lowest point reached by the market in those 12 months, while the grey bars represent the full year’s return. While market pullbacks are a normal part of investing, history shows that in most years, markets still finish in positive territory. Double-digit declines may occur, but they’re often followed by strong recoveries. Rather than trying to predict short-term dips, investors should stay focused on long-term goals.

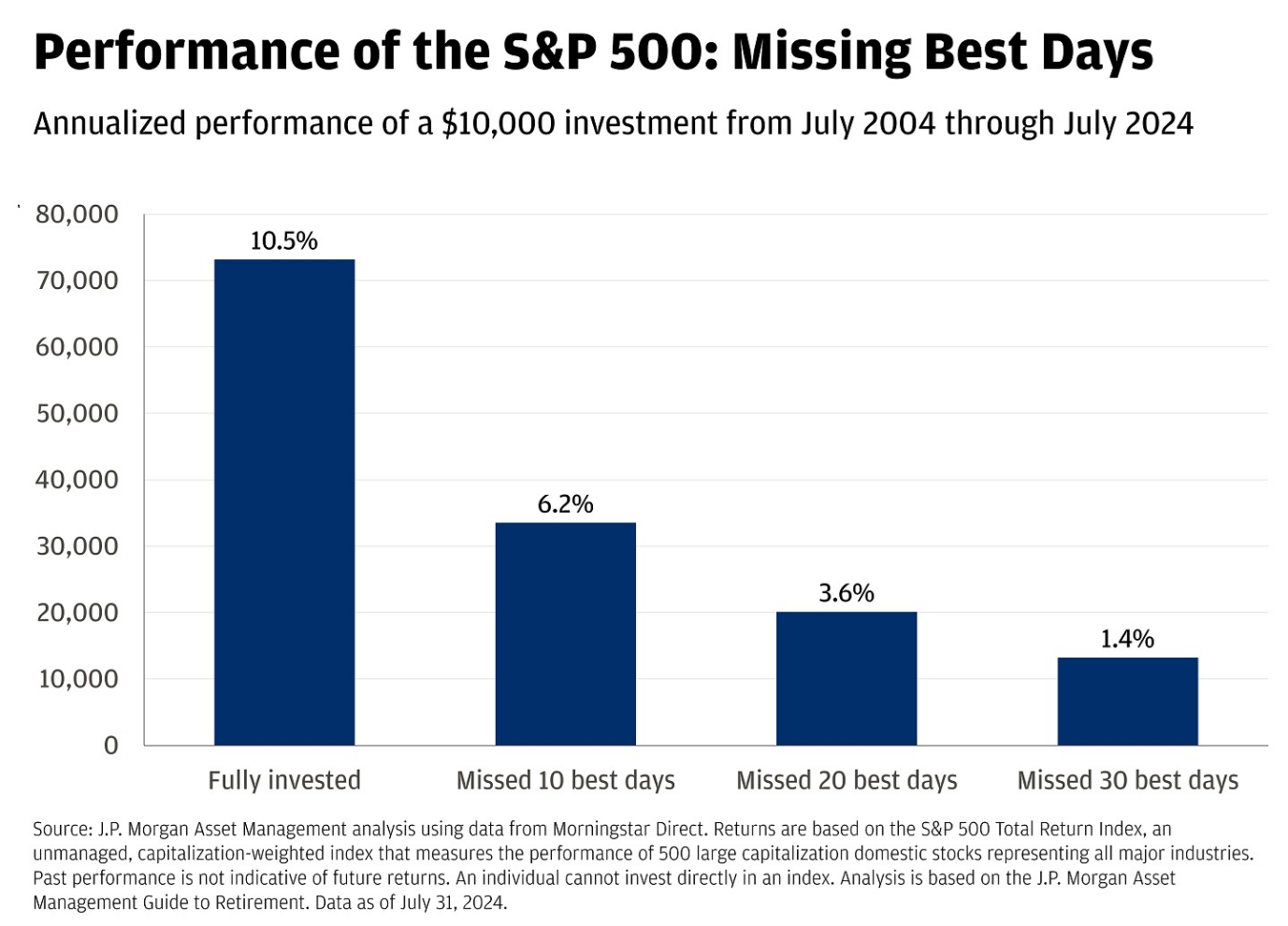

An analysis of stock market returns over a 20-year time period shows the power of remaining invested and not trying to time the market. Using data from the US S&P 500 market, the chart below shows the enormous cost of missing just a handful of the best trading days over the period, which encompasses the global financial crisis, Covid and numerous other notable market events.

If you were to put $10,000 into the S&P 500 in 2004 and stay fully invested through to the middle of 2024, you would have over $70,000. If you missed just the 10 best trading sessions though, you would be left with under $35,000. The reason? Market timing is incredibly difficult. Over the last 20 years, seven of the 10 best days occurred within 15 days of the 10 worst days.

Whilst the chart below illustrates values in US dollars, the same principles apply to pounds sterling. If you were to invest £10,000 in the S&P 500 in 2004 and stay fully invested through to the middle of 2024, you would have over £70,000. However, if you missed just the 10 best trading sessions, you would be left with under £35,000. The reason? Market timing is incredibly difficult. Over the last 20 years, seven of the 10 best days occurred within 15 days of the 10 worst days.

One of the smartest strategies for managing risk is diversification. Spreading your investments across various asset classes, sectors, and global markets. A well-diversified portfolio acts as a cushion during volatile periods, with strong-performing assets often helping to offset areas of your portfolio that are not delivering as strong rewards.

This balanced approach allows investors to ride out market fluctuations while still being positioned for long-term growth.

The evidence is clear: staying invested through the ups and downs of the market leads to stronger outcomes over time. Long-term investing rewards patience, discipline, and consistency. It also allows you to take advantage of powerful benefits such as compounding, tax efficiencies, and the natural rebound of economies.

It’s perfectly reasonable to keep some cash on hand for short-term needs. But for your longer-term goals, whether it’s retirement, buying a home, or leaving a legacy, the best approach is to remain invested in a strategy that aligns with your personal risk profile and objectives.

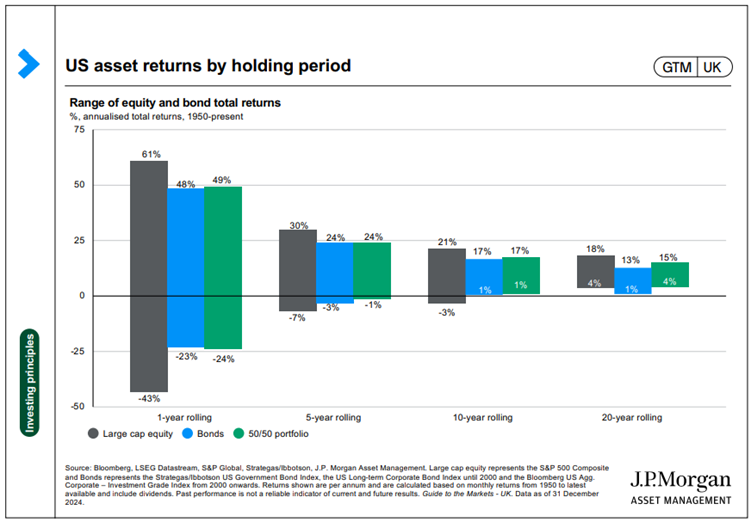

As this final chart shows, using representative data from US markets that read across directly to UK investors, while markets can always have a bad day, week, month or even a bad year, history suggests investors are much less likely to suffer losses over longer periods. It’s important to keep a long-term perspective. Investors should not necessarily expect the same rates of return in the future as we have seen in the past, but a diversified blend of stocks and bonds has not suffered a negative return over any 10-year rolling period historically, despite the great swings in annual returns we have seen since 1950:

Attempting to predict market movements often leads to missed opportunities. Staying consistently invested allows you to benefit from long-term growth and recovery periods.

Market downturns are inevitable, but history shows they are usually short-lived. Maintaining your investment strategy during turbulent times is more effective than reacting emotionally.

Even missing a few top-performing days can drastically reduce long-term returns. A disciplined, stay-the-course approach typically outperforms panic selling.

A well-diversified portfolio across asset classes, sectors, and regions—mitigates risk and provides stability during market swings.

Sticking with your investment plan through economic cycles harnesses the power of compounding and positions you for greater financial security over time.

If you’re looking to revisit your financial plan or explore new investment opportunities, we’re here to guide you. Our team can offer personalised advice and insights tailored to your unique circumstances, helping you navigate uncertainty with confidence.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

Every year, billions of pounds in unpaid taxes deprive the UK’s public services of crucial funding. To tackle this issue, Chancellor Rachel Reeves has unveiled an ambitious strategy to close the tax gap, ensuring a fairer system where individuals and businesses contribute their fair share. With measures projected to generate over £1 billion annually by 2029/30, the government is ramping up enforcement, digitalisation, and anti-avoidance efforts to create a more equitable tax landscape.

The scale of unpaid tax in the UK is staggering. By December 2024, HMRC reported tax debt exceeding £44 billion—more than double the figure from five years ago. Shockingly, around £20 billion of this debt is over a year old, making recovery increasingly difficult.

To combat this crisis, the government is enhancing HMRC’s capabilities with a targeted debt recovery programme. This includes:

A major pillar of reform is the continued rollout of Making Tax Digital (MTD), designed to simplify tax management for individuals and businesses. From April 2028, sole traders and landlords earning over £20,000 will be required to use MTD for income tax Self Assessment (ITSA).

For smaller taxpayers earning below the MTD threshold, the government is working on enhancing reporting systems to ease compliance. Additionally, stricter penalties for late payments on VAT and ITSA will reinforce timely submissions, reducing the risk of tax shortfalls.

The government is intensifying efforts to combat tax avoidance and fraudulent schemes, with a focus on:

As part of a new tax fraud initiative, HMRC aims to increase criminal prosecutions, particularly targeting wealthy individuals, corporate fraud, and offshore tax evasion. By 2029/30, HMRC plans to process 600 serious tax fraud cases annually, up from 500 today.

To further strengthen compliance, HMRC is revamping its whistleblower reward scheme, offering financial incentives linked to tax recovered from tip-offs. Inspired by successful models in the US and Canada, this initiative aims to target large-scale tax evasion.

Additionally, a joint task force with HMRC, Companies House, and the Insolvency Service is tackling ‘phoenixism’—a practice where businesses dissolve to avoid tax liabilities. New measures include:

The government is also reinforcing offshore tax compliance by investing in AI, data analytics, and private sector expertise. These advancements will help HMRC detect hidden wealth and recover an estimated £500 million in offshore tax revenue over the next five years.

Further modernisation efforts include:

These reforms mark a crucial step toward closing the UK’s tax gap, ensuring fair contributions from all taxpayers while safeguarding essential public funding. By embracing digitalisation, enhancing enforcement, and cracking down on tax avoidance, the government is creating a tax system that is both fair and future-ready.

With HMRC’s transformation roadmap expected this summer, businesses and individuals can anticipate a streamlined, transparent tax framework designed to support economic growth and financial integrity across the UK.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

THIS ARTICLE DOES NOT CONSTITUTE TAX, LEGAL OR FINANCIAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

Chancellor Rachel Reeves said that the Office for Budget Responsibility (OBR) has downgraded growth projections for 2025 but has upgraded forecasts for every year thereafter for the remainder of this parliament. She told MPs: ‘There are no shortcuts to economic growth. It will require long-term decisions. It will demand hard work. It will take time for the reforms we are implementing to have an impact on the everyday economy.’

Our Guide to Spring Forecast Statement 2025 summarises the key points announced.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

THIS ARTICLE DOES NOT CONSTITUTE TAX, LEGAL OR FINANCIAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

Chancellor Rachel Reeves has outlined a transformative vision for Britain’s future, anchored in the government’s Plan for Change. This strategy is designed to drive economic growth, strengthen the National Health Service (NHS), and reinforce national security—all while maintaining financial stability.

Last autumn’s Budget marked a significant fiscal reset, ensuring a sustainable financial future for the UK. The government tackled £22 billion in financial pressures, introduced groundbreaking tax reforms, and implemented strong fiscal rules to protect working households. These decisive measures have safeguarded public finances while enabling vital investments in public services and economic growth.

The Chancellor reaffirmed the government’s commitment to supporting working families, citing last year’s National Minimum Wage increase and fuel duty freeze. These policies have already had a tangible impact, with the Bank of England reducing interest rates three times since the start of the parliamentary term. By the end of 2024, real wages are expected to rise at their fastest pace in over three years, alleviating the cost-of-living pressures on millions.

Despite global economic challenges—ranging from geopolitical tensions in Europe to rising borrowing costs—the UK remains resilient as a leading trading economy. The Chancellor assured that, despite these headwinds, Britain is well-positioned to navigate uncertainty and sustain long-term growth.

Economic forecasts now suggest Britain will outpace previous growth predictions from 2026 onwards. Thanks to decisive action, the government has met its fiscal targets two years ahead of schedule, maintaining a balance between financial discipline and pro-growth policies.

With a solid foundation in place, the government is adopting bold measures to boost public services, economic expansion, and national security. This includes a strong focus on protecting working families’ financial futures and fortifying the country’s long-term prosperity.

A key announcement in the Spring Statement is the government’s fully funded commitment to increasing defence spending. By 2027, defence expenditure will reach 2.5% of GDP, with an extra £2.2 billion allocated to the Ministry of Defence (MOD) next year alone. This investment reinforces the UK’s global security leadership and strengthens its partnerships with NATO allies.

Additionally, the government is reforming public services to improve efficiency while ensuring that welfare spending reaches those who need it most. Enhancing tax collection efforts will also help ensure tax fairness and bolster public finances.

Investment is central to the Plan for Change. Over the next five years, the government is committing £13 billion to infrastructure projects and launching a construction skills initiative to train 60,000 new workers. A further £2 billion is earmarked for social and affordable housing, addressing the UK’s housing crisis.

Major planning reforms will also drive economic expansion. Updates to the National Planning and Policy Framework (NPPF) are expected to lead to the construction of 170,000 additional homes, adding £6.8 billion to the economy by 2029/30. By 2034/35, GDP growth from these reforms could exceed 0.4%—all at no direct fiscal cost.

These reforms will also have a broader economic impact. By 2029/30, they are projected to reduce public borrowing by £3.4 billion, strengthening the UK’s financial stability. The government’s approach—focused on capital investment, regulatory improvements, and the proposed Planning and Infrastructure Bill—demonstrates a clear commitment to sustainable growth.

The Chancellor’s Plan for Change is more than a response to today’s challenges; it is a roadmap for a thriving, inclusive, and globally competitive Britain. Through a combination of fiscal responsibility, strategic investment, and innovative reform, the UK is poised for long-term success.

With a vision that balances short-term relief with long-term stability, the government is setting the stage for a prosperous future—one where working families, businesses, and public services all benefit.

This bold and decisive agenda will shape Britain’s economic future, ensuring stability, security, and sustained growth for generations to come.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

THIS ARTICLE DOES NOT CONSTITUTE TAX, LEGAL OR FINANCIAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

The UK’s latest economic forecast may point to slower growth in the short term, but it’s far from a reason to worry. In fact, now is a great time to review your financial goals and make sure your plans are working as hard as they can for you. With a clear view of where we’re headed – and what steps to take – individuals, families, and business owners alike can move forward with confidence.

Chancellor Rachel Reeves has announced that UK growth is expected to come in at 1% in 2025, lower than the previous forecast of 2%. While this indicates a more cautious short-term outlook, the longer-term projections remain steady, with growth expected to pick up to 1.9% in 2026 and stay close to that level in the following years.

The government has already begun introducing reforms designed to stimulate long-term economic growth. These include bold new housebuilding targets – aiming for the highest level of construction in four decades – and planning reforms to help unlock land for development.

What does that mean for you?

Recent tariff announcements by the U.S. administration have contributed to renewed volatility across global markets. While these developments may feel unsettling, it’s important to stay grounded.

At Fairstone, we understand that short-term market fluctuations are part of the journey and reacting to peak uncertainty often leads to poor investment outcomes. That’s why we maintain a disciplined, long-term investment philosophy focused on diversification, high-quality assets, and strategic planning.

We strongly encourage investors to avoid knee-jerk decisions in response to headlines. Staying committed to your long-term investment strategy is typically the most reliable path through periods of volatility.

Inflation remains a factor, with the OBR forecasting it at 3.2% this year. However, it’s expected to fall back towards the Bank of England’s 2% target over the next couple of years – good news for household budgets.

Meanwhile, real household disposable incomes are forecast to rise, thanks in part to stronger-than-expected wage growth. On average, households could be around £500 better off per year compared to previous projections.

Like all major economies, the UK isn’t immune to global risks – from geopolitical tensions to shifting trade dynamics. However, the government has reaffirmed its commitment to maintaining fiscal stability and creating a more resilient economy for the future.

Here’s what you should take away

The growth figures might not be as high as hoped – but this is not a time for pessimism. It’s a chance to take stock, make smart financial decisions, and position yourself to benefit from the UK’s long-term recovery.

If you’re unsure how these changes affect your personal or business finances, we’re here to help.

THIS ARTICLE DOES NOT CONSTITUTE TAX, LEGAL OR FINANCIAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

The clock is ticking. As the tax year-end approaches, UK investors have a golden opportunity to make the most of their tax-free savings’ allowance. If you haven’t yet considered a Stocks & Shares ISA, now’s the time to take action. This isn’t just another savings account; it’s a powerful tool to grow your wealth without the burden of taxes.

Imagine investing in the stock market and keeping every penny of your profits. That’s exactly what a Stocks & Shares ISA allows you to do. Any capital gains you make within your ISA are completely free from Capital Gains Tax (CGT) which could otherwise take up to 24% of your profits. [1] Source: HMRC, 2024.

Dividends are also tax-free. If you hold shares outside an ISA, you’ll pay dividend tax once you go over the £500 annual allowance (down from £1,000 in 2023). Within an ISA, there’s no tax bill. (Source: HMRC, 2024)

And if your ISA investments include bonds or other interest-bearing assets, the interest earned is free from Income Tax, meaning more money stays in your pocket.

Each tax year, you can invest up to £20,000 in an ISA. If you don’t use your full allowance by April 5th, you lose it forever. You can’t roll it over. That’s why savvy investors make sure they top up their ISA before the deadline. Over time, consistently maxing out your ISA allowance can result in substantial tax-free savings. Just look at the numbers: if you invest £20,000 annually for 20 years and achieve a 6% average return, you could be sitting on over £730,000 completely tax-free.

While a Cash ISA might offer security, most accounts struggle to keep up with rising costs. The latest figures show the UK’s inflation rate hovering around 4% (Source: ONS, 2024), while many Cash ISAs offer interest rates below this. In contrast, stock market investments have historically delivered average annual returns of 7-10% over the long term.

Of course, investing in the stock market carries risks, and short-term dips are inevitable. But over a five- to ten-year period, a diversified Stocks & Shares ISA has the potential to significantly outperform cash savings.

One of the biggest advantages of an ISA is its set-and-forget nature. You don’t have to worry about filling out self-assessment tax returns for gains, dividends, or interest. Unlike other investments, everything stays tax-free and hassle-free.

And let’s not forget the power of compounding. When you reinvest dividends and profits within an ISA, your money grows at an accelerating rate, helping you build wealth faster. The longer you leave it, the more your investments can snowball.

Stocks & Shares ISAs aren’t just for the here and now; they’re a fantastic tool for long-term wealth planning. Whether you’re saving for retirement, a property, or simply financial freedom, this tax-efficient vehicle can help you get there faster. And if you’re married or in a civil partnership, you can pass your ISA onto your spouse tax-free when you die, ensuring your investments continue to benefit your loved ones.

Don’t let your £20,000 allowance go to waste. If you’re already investing, consider topping up before 5 April.

If you’re unsure where to begin, speak to a financial adviser. Whatever you do, don’t let this tax-efficient opportunity slip away.

THIS ARTICLE DOES NOT CONSTITUTE TAX, LEGAL OR FINANCIAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

A PENSION IS A LONG-TERM INVESTMENT NOT NORMALLY ACCESSIBLE UNTIL AGE 55 (57 FROM APRIL 2028 UNLESS THE PLAN HAS A PROTECTED PENSION AGE).

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

YOUR PENSION INCOME COULD ALSO BE AFFECTED BY THE INTEREST RATES AT THE TIME YOU TAKE YOUR BENEFITS.

I’ve always believed in the power of New Year’s resolutions. Over the years, I’ve seen first hand how sticking to well informed financial commitments can transform people’s lives, not only in terms of wealth, but in their overall sense of security and confidence. Building a stronger portfolio is similar to many other long-term goals, like buying a home or securing a comfortable retirement, those who embrace financial resolutions consistently see progress in their portfolio and a strong foundation for their future.

By committing to a few smart resolutions and sticking with them, you’ll set a strong foundation for the years to come. Whether you’re just starting your investment journey or looking to refine your approach, these are the steps that I think investors should take to help take control of your finances and move closer to the life you want.

Consistency is one of the most powerful habits in investing. By contributing to your portfolio regularly, even when markets are unpredictable, you can benefit from pound cost averaging. This strategy helps smooth out the ups and downs of the market over time.

Make it easy by automating your contributions. Whether you’re investing large sums or starting small, the key is building the habit and staying consistent. And if you have any unused cash in your portfolio, ensure it’s put to work in your chosen assets, so every penny contributes to your financial growth.

It’s easy to get frustrated when markets fluctuate. Maybe you’ve seen a share price dip and second-guessed your decisions, but that’s usually just temporary sentiment at work. Even solid companies can see their stock values drop due to short-term market conditions or broader trends.

The key is focusing on the bigger picture. History shows that markets recover, and patience often turns perceived losses into gains. The real secret to success? It’s not about timing the market but spending time in it. Stick to your strategy, trust the fundamentals of your investments, and resist the urge to react to every market hiccup.

Many UK investors stick close to home, but the global market offers so much more. Did you know that the UK makes up just 4% of the world’s equity markets? That leaves a massive 96% of opportunities waiting to be explored.

By diversifying your portfolio beyond the UK, you can tap into differentiated markets like the US, Europe, and even emerging economies. The world is full of possibilities—don’t miss out by keeping all your investments local.

While it’s smart to let your investments grow without constant tinkering, an annual check-in is essential. What worked for you a few years ago might not align with your goals or the current economic environment today. Inflation, global trends, and personal milestones all play a role in shaping your financial needs.

Take time to review your investment portfolio management and make sure it’s on track. You might consider rebalancing your assets, exploring fee-free platforms, or even switching to a managed portfolio for professional guidance. Staying proactive ensures your investments remain aligned with your evolving goals.

A well-rounded investment approach starts with gathering insights from a variety of trusted sources, whether website or news outlets. While personal research is essential, broadening your network to include industry leaders and financial experts can give you a clearer, more comprehensive understanding of the markets. Many professionals regularly share valuable advice on market trends, investment strategies, and portfolio management—resources that can help refine your own decisions.

At the same time, it’s crucial to challenge your assumptions by seeking out alternative views. Avoid the trap of “confirmation bias,” where you only focus on information that supports your existing beliefs. Instead, leverage a diverse range of insights to ensure your portfolio remains balanced and forward-looking.

For those seeking a deeper level of expertise, working with a wealth manager can be a natural next step. Professional advisers provide tailored strategies, objective advice, and access to advanced tools that can enhance your financial plan. By combining your independent research with expert guidance, you can optimise your portfolio for long-term success and greater peace of mind.

Market fluctuations are normal, and even strong companies can experience temporary price dips. Focus on the bigger picture:

The UK represents just 4% of the global equity market, leaving 96% of opportunities in regions like the US, Europe, and emerging markets. Diversifying globally can:

Consistency in investing allows you to benefit from pound cost averaging, which smooths out market volatility over time.

An annual review helps ensure your investments align with your financial goals and the current market environment. Consider:

________________________________________

Emerging markets can offer significant growth opportunities but also come with higher risks. Diversify wisely and consider these investments as part of a balanced portfolio.

To combat inflation:

Explore ESG (Environmental, Social, and Governance) investments to align your portfolio with your values. Many platforms now offer tools to screen for sustainable or ethical investment options.

It’s never too late to begin. Even small contributions over time can significantly grow thanks to compounding. The key is to start where you are and remain consistent.

While it’s possible to manage your investments independently, a financial adviser can offer:

The habits you build today will shape your financial future. By diversifying globally, investing consistently, and focusing on the long term, you’ll set yourself up for success. Take the time to review and refresh your portfolio so that it’s working as hard as you are.

Start now, and 2025 could be your most rewarding financial year yet.

| Match me to an adviser | Subscribe to receive updates |

THIS ARTICLE DOES NOT CONSTITUTE TAX OR LEGAL ADVICE AND SHOULD NOT BE RELIED UPON AS SUCH. TAX TREATMENT DEPENDS ON THE INDIVIDUAL CIRCUMSTANCES OF EACH CLIENT AND MAY BE SUBJECT TO CHANGE IN THE FUTURE. FOR GUIDANCE, SEEK PROFESSIONAL ADVICE.

A PENSION IS A LONG-TERM INVESTMENT NOT NORMALLY ACCESSIBLE UNTIL AGE 55 (57 FROM APRIL 2028 UNLESS THE PLAN HAS A PROTECTED PENSION AGE).

THE VALUE OF YOUR INVESTMENTS (AND ANY INCOME FROM THEM) CAN GO DOWN AS WELL AS UP, WHICH WOULD HAVE AN IMPACT ON THE LEVEL OF PENSION BENEFITS AVAILABLE.

YOUR PENSION INCOME COULD ALSO BE AFFECTED BY THE INTEREST RATES AT THE TIME YOU TAKE YOUR BENEFITS.