March 2026 will be remembered as one of the most volatile months in recent market history, and it all came down to what was happening in the Middle East. The conflict involving the US, Israel, and Iran escalated dramatically during the month, culminating in the closure of the Strait of Hormuz—one of the world’s most critical oil and gas shipping routes. This wasn’t just a geopolitical headline; it had immediate and severe consequences for global energy markets.

Oil prices surged as cargo flows through the strait were disrupted, sending shockwaves through supply chains worldwide. The energy shock was swift and brutal, with petroleum products leading the charge higher. By mid-March, the situation looked increasingly dire, with the US deploying three additional warships and more Marines to the region around March 20th, which only added to market anxiety.

However, as March drew to a close and we moved into April there were some tentative signs of hope as a fragile ceasefire agreement was reached between the two sides, resulting in a very strong, positive market reaction. The ceasefire is planned to last for two weeks with US and Iranian negotiators meeting from Friday 10th April.

While the situation undoubtedly remains fluid and uncertain, this shift in tone has helped to ease some of the panic that had gripped markets earlier in the month. Still, some damage has been done—energy costs have already spiked, inflation has started to trend higher, all of which leaves the world’s central banks caught between a rock and a hard place.

Central bankers had a truly miserable March, caught in a classic policy bind: fight inflation caused by an energy shock, or protect economic growth that’s already looking fragile?

The whiplash in market expectations told the story. The Federal Reserve held rates steady at 3.75% and spoke about “looking through” the energy shock, while the Bank of England took a tougher line, saying it “stands ready to act” against inflation in its first unanimous vote in four and a half years. The European Central Bank were the most explicit, speaking of standing ready to raise interest rates if needed to combat inflation. Here, rate hike expectations swung wildly from fully priced to just 50-50 odds by the month-end.

All that uncertainty wasn’t happening in a vacuum—inflation data was trending higher. The euro area saw its biggest jump in inflation since 2022, rising to 2.5% year-over-year in March from 1.9% in February. Germany hit 2.8% as energy costs rocketed 7.2% higher, while French inflation nearly doubled from 0.9% to 1.7% in a single month. Even US wholesale prices accelerated unexpectedly, rising 0.7% month-over-month in February—before the worst of the energy shock hit.

With all this uncertainty swirling around—war, inflation, confused central banks—it’s no surprise that stock markets had a very weak March. For UK investors, despite a weaker pound helping translated equity returns, losses were painful across the board.

The US outperformed other regions handily over the month with the S&P 500 falling by 3.3% and the NASDAQ by just under 3% (green and pink lines respectively in the chart below), as investors judged the region to be relatively insulated to the energy price shocks versus other regions as a massive producer of oil and gas.

Elsewhere there was little good news as developed and emerging market regions struggled to a greater or lesser extent. The FTSE 100 fell by 6.7% (light orange line), European equities by more than 9% (light purple line), and Japanese stocks (blue line) by nearly 11.5%.

Emerging markets bore the brunt of the sell-off, (yellow line) with the region typically more sensitive to energy shocks and tending to suffer more when global growth looks shaky. The worst of the equity selling came around March 20th when news broke about additional US military deployments to the Middle East. That triggered a large risk-off move, with investors dumping stocks and fleeing to safety.

There was a brief rally attempt right at the end of the month and into early April as ceasefire hopes emerged, but that came too late to salvage March’s performance.

Government bond yields swung wildly as investors tried to figure out whether inflation or recession was the bigger threat.

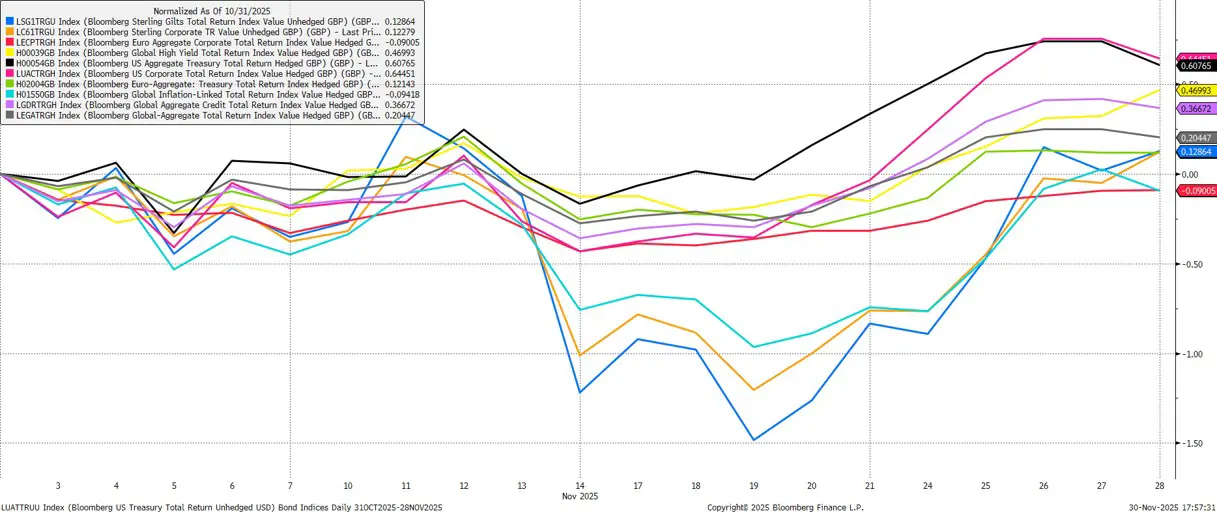

Sterling assets and particularly UK Gilts had a wild ride as investors judged the UK economy and UK assets to be at heightened risk from higher energy prices and inflation. The 10-year Gilt yield started March around 4.37%, then surged to nearly 5.00% on March 20th after the Bank of England’s hawkish turn; a very large move in a short space of time. Yields fell slightly into the end of the month but per the chart below (blue line) Gilts ended the month down more than 4% in price terms.

US Treasuries followed a similar pattern. The 10-year yield climbed from about 4.04% at the start of March to a peak of 4.43% on March 27th, before ending at 4.32%. This equated to a benchmark index loss of around 1.7% (black line).

The pattern was consistent: inflation fears drove yields sharply higher in the first three weeks of March, then growth concerns brought them back down a bit in the final week. For bond investors, it was an exhausting month of trying to anticipate which risk would dominate.

In currency markets, sterling had a mixed month, with performance delineated by investors’ perceptions of the Middle East crisis impact. Most notably, the pound fell sharply against the US dollar (green line) by 1.9% which reflected a flight to dollar safety. The greenback benefitted from its traditional safe-haven status despite the Fed’s cautious policy stance, with dollar strength pervasive across the complex.

The currency moves underscored how, in times of genuine crisis, traditional safe-haven flows can trump interest rate differentials—even the BoE’s hawkish rhetoric couldn’t prevent sterling from weakening as investors prioritised capital preservation over yield:

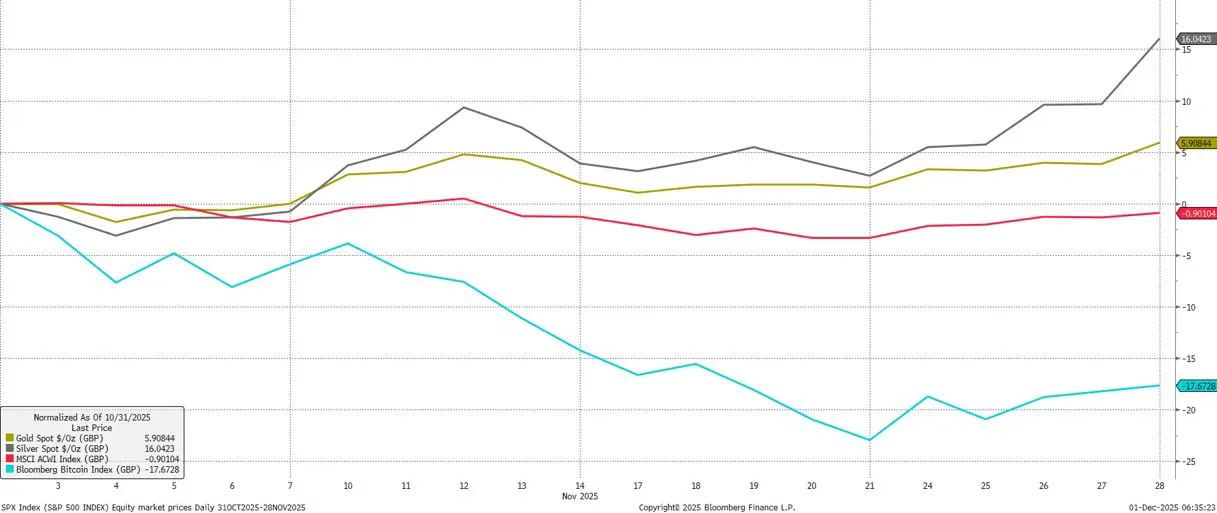

The precious metals complex had a surprisingly rough month, defying their traditional safe-haven status. Gold fell for nine consecutive days during the month as inflation fears and expectations for higher interest rates outweighed safe-haven demand. The metal tumbled from highs above $5,350 per ounce in early March to intra-day lows near $4,100, before recovering somewhat to end the month around $4,680.

Silver was hit even harder, tumbling more than 10% at one point on March 23rd and falling from nearly $89 per ounce to lows around $67, before ending March at approximately $75. The selloff reflected the fact that rising real interest rates are a headwind for non-yielding precious metals, even in times of geopolitical stress.

As we move through April, uncertainty remains with us. A fragile ceasefire has been agreed in the Middle East which would be hugely positive if it holds. But central banks are still stuck in a tricky position, trying to balance inflation risks against growth concerns.

We think it’s sensible to expect continued volatility in equity markets until we get more clarity on both the geopolitical situation and what central banks are actually going to do. On that latter point, the next few weeks will be crucial. Central banks meet again in late April, and we’ll get more clarity on whether the Middle East situation is truly stabilising or just in a temporary lull. The tug-of-war between inflation control and growth preservation will likely determine where markets go from here.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

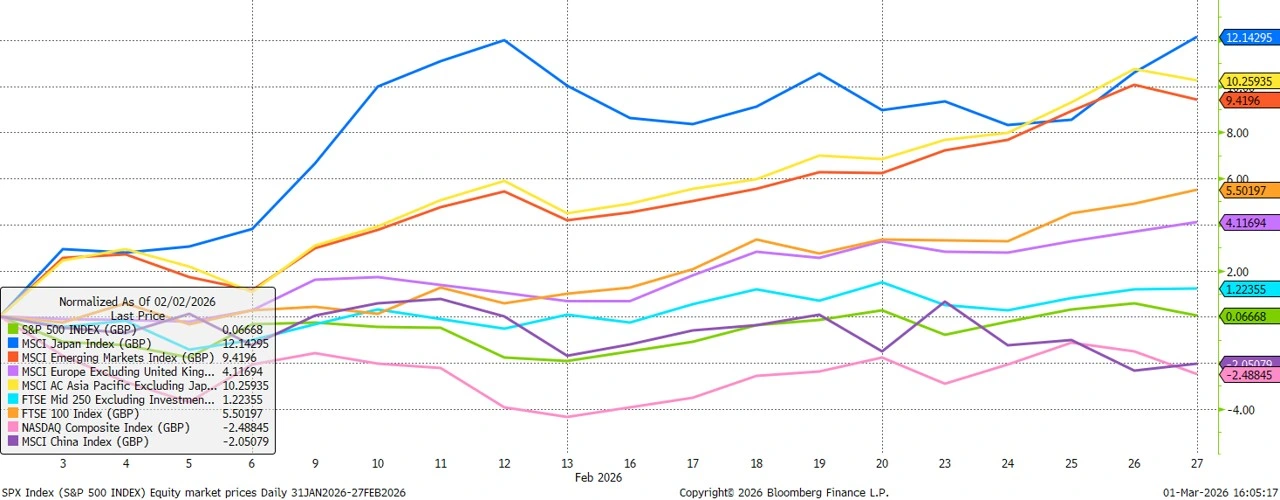

February proved to be a month of stark regional divergence across global equity markets, punctuated by a landmark US Supreme Court ruling that reshaped the tariff landscape, and escalating geopolitical tensions in the Middle East. For UK investors, sterling weakness against most major currencies added an additional layer of complexity to portfolio positioning.

In GBP terms, Asian markets delivered exceptional performance during February, with Japan’s equity market surging 12.1% to claim the top spot among major regional indices. The Nikkei 225 reached a historic milestone of 59,000, propelled by Prime Minister Sanae Takaichi’s growth-oriented policies following her election victory. Foreign investors responded enthusiastically, purchasing a net ¥1.78 trillion ($11.5 billion) in Japanese shares and futures in the week ended February 13—the largest inflow since November 2014. Japanese chipmakers, defence contractors, and materials producers led the rally, with the top three performers in the MSCI World Index all being Japanese firms.

The broader Asian story was equally compelling. Asia ex-Japan gained 10.3%, posting its best February on record as investors piled into companies supplying artificial intelligence infrastructure. South Korea’s technology giants Samsung Electronics and SK Hynix reached a combined market capitalization of $1.14 trillion, surpassing China’s Alibaba and Tencent at $1.07 trillion—a symbolic shift underscoring how the AI boom has reshaped investment dynamics across the region.

By contrast, US equities struggled again. The S&P 500 Index gained a mere 0.1% in GBP terms, weighed down by a rotation away from mega-cap technology stocks as artificial intelligence enthusiasm cooled:

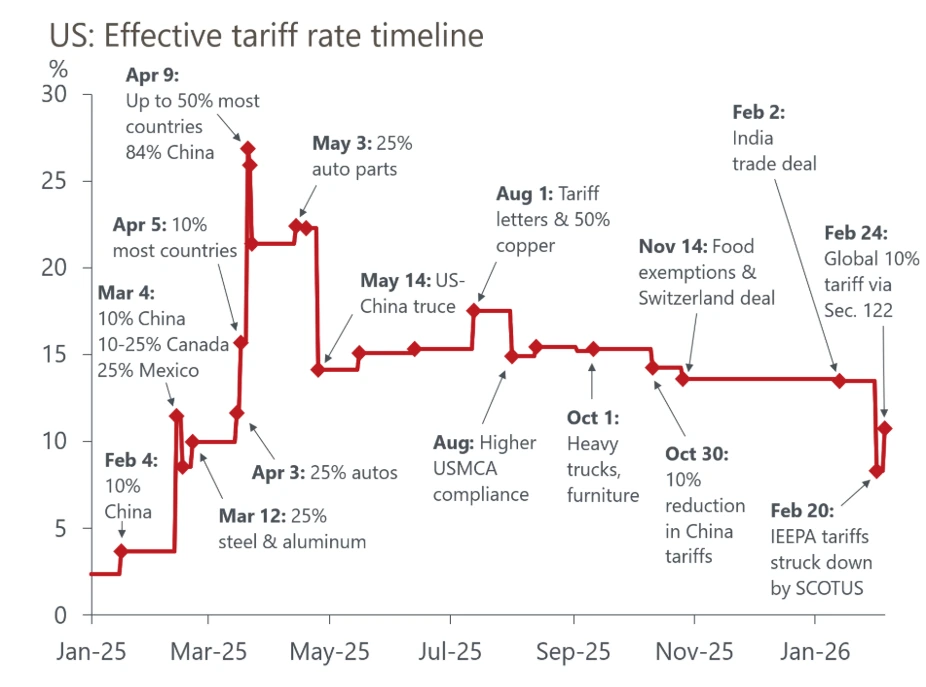

The month’s most significant policy development came on February 20, when the US Supreme Court struck down President Trump’s sweeping global tariffs in a 6-3 decision. Chief Justice John Roberts, writing for the majority, ruled that Trump had exceeded his authority by invoking the International Emergency Economic Powers Act (IEEPA) to impose “reciprocal” tariffs, stating that the Constitution reserves the authority over taxes and tariffs for Congress.

The immediate impact was substantial: the US effective tariff rate fell from 13.6% to 6.5%, with China emerging as a significant beneficiary as its fentanyl-linked and reciprocal tariffs were invalidated. Markets rallied on the news, with European shares hitting an all-time high and the S&P 500 rising as much as 0.7%:

However, the relief proved short-lived. President Trump immediately announced plans to impose a 10% global tariff under Section 122 of the 1974 Trade Act, later raised to 15%, effective for 150 days. Treasury Secretary Scott Bessent assured markets that tariff revenue would be “virtually unchanged” in 2026 as the administration invoked alternative legal authorities. The ruling also opened the door to a potentially prolonged battle over refunds, with as much as $170 billion in already-collected tariffs now subject to legal challenge.

UK investors faced headwinds from sterling weakness, which depreciated against all major developed and emerging market currencies during February. The pound fell by 1.5% against the euro, touching its lowest level in more than two months, and against the US dollar, sterling lost 1.3%, snapping a three-month winning streak.

The catalyst for sterling’s decline was twofold. First, the Bank of England came unexpectedly close to cutting interest rates, with a 5-4 split among rate-setters in favour of holding at 3.75%—far closer than the 7-2 outcome economists had anticipated. This fuelled bets on a March rate cut, with traders pricing roughly 60% probability. Second, domestic political turmoil intensified following various government scandals through the month, along with a Green Party by-election victory in Manchester, amplifying speculation about Keir Starmer’s future:

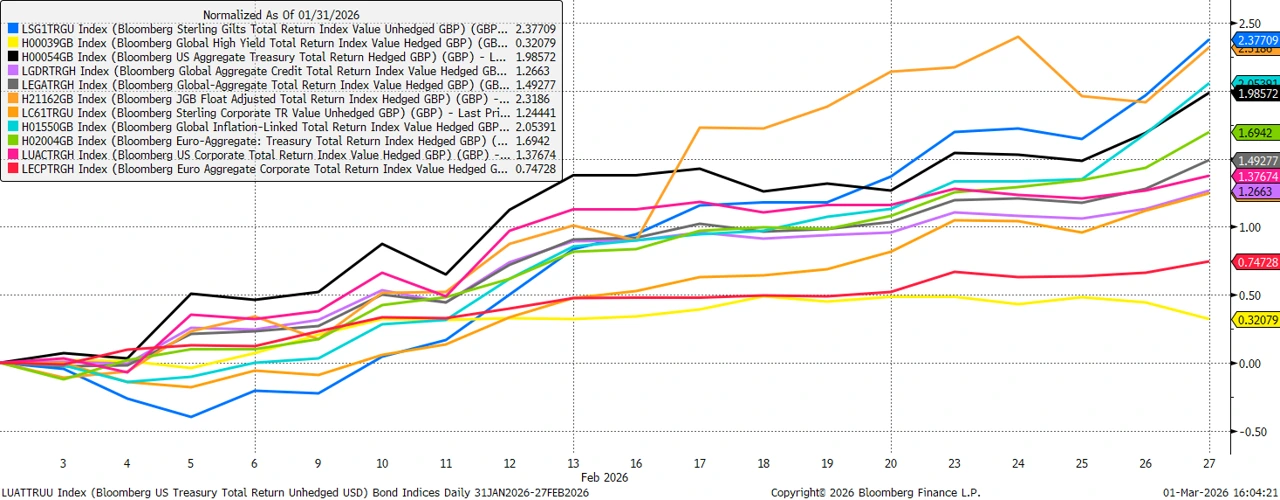

Bond markets reflected growing risk aversion, with government bonds strongly outperforming corporate bonds. UK Gilts delivered particularly strong returns, rising by 2.4% over the month following the BOE’s close rate vote, and as haven demand intensified amid souring sentiment toward risky assets.

US Treasuries rallied sharply as well, with the 10-year yield falling below 3.96%—the lowest in 6 months—and the 2-year yield reaching its lowest level since August 2022 at 3.37%.

UK gilts declined 6.1% in GBP terms despite initial gains The yield curve steepened as front-end gilts rallied on rate cut expectations while longer-dated bonds sold off on supply concerns.

Corporate bond markets proved resilient though less positive, the global high yield index rising by 0.3% over the month, reflecting continued risk appetite despite equity market volatility.

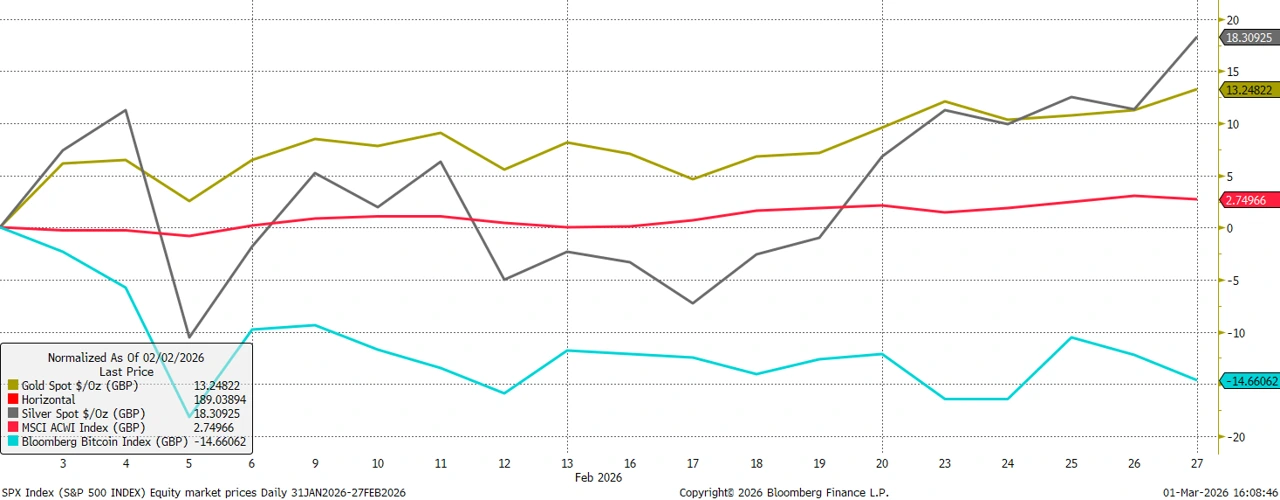

Precious metals posted yet more remarkable performance in February. Silver led the way with an 18.3% gain in GBP terms, extending its winning streak to 10 consecutive months, while gold advanced by 13.2%, posting one of its biggest monthly increases since January 2012.

The rally was driven by a combination of factors: early-month volatility that saw both metals register sharp drawdowns before dip-buyers returned, sustained retail demand despite price swings, and escalating geopolitical tensions as the month drew to a close:

The month ended with a dramatic escalation in Middle East tensions that has continued to dominate headlines into early March. On 1st March, Iran’s supreme leader Ayatollah Ali Khamenei was killed in coordinated US-Israeli airstrikes, marking a significant intensification of the conflict spiralling across the oil-rich region. President Trump stated that “heavy and pinpoint bombing” would continue throughout the week, while Iran responded with retaliatory missile attacks on Gulf nations.

The conflict has already begun disrupting traffic around the Strait of Hormuz, the critical shipping chokepoint through which roughly one-fifth of the world’s oil and liquefied natural gas flows. Oil prices, which had settled at around $73 per barrel before the attacks, have risen sharply through the first week of March, as investors assess and price in the higher risks to global energy supply.

The conflict introduces the risk of a prolonged period of elevated oil prices feeding through to broader inflation, potentially forcing central banks to maintain restrictive policy for longer than previously anticipated, or in a worst-case scenario, even consider tightening further despite slowing growth.

As we move into March, several themes warrant close attention. The durability of Asian equity outperformance will depend on whether AI infrastructure demand remains robust. The tariff landscape remains fluid, with the 150-day clock ticking on Trump’s Section 122 levies and ongoing legal battles over refunds. Sterling’s trajectory will hinge on BOE policy decisions and domestic political stability. Most critically, the Middle East conflict introduces significant uncertainty around oil prices and inflation, with potential ramifications for central bank policy globally.

For us as UK-based investors, February’s divergent performance across regions and asset classes underscores the importance of diversification and active currency management in navigating an increasingly complex global landscape.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

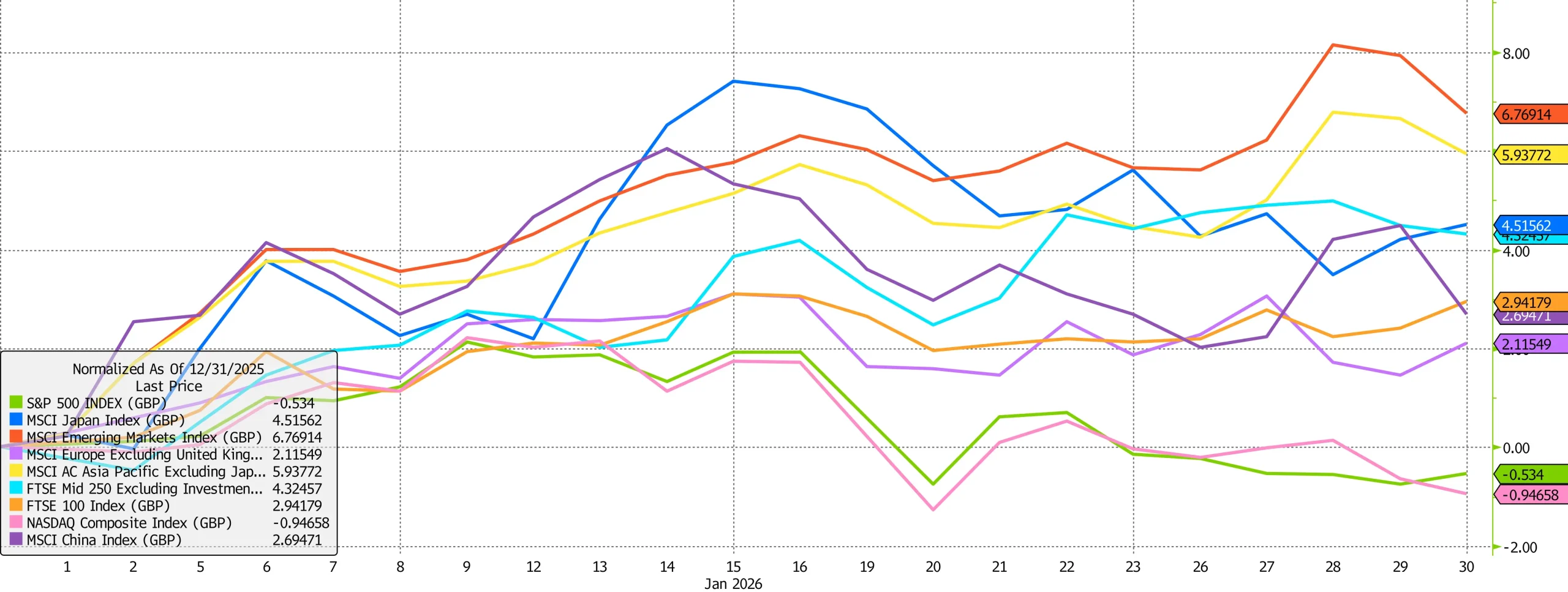

Global markets began 2026 on a broadly constructive footing, with January delivering positive returns across most major asset classes despite an ongoing backdrop of macroeconomic, political, and geopolitical uncertainty. Rather than a simple risk-on or risk-off environment, market outcomes were shaped by pronounced rotation across regions, styles, currencies, and asset classes. Leadership continued to broaden beyond the narrow concentration that defined much of the past two years, while bond markets reflected growing divergence across sovereign curves and credit sectors.

Source: Bloomberg

Global equities advanced meaningfully during the month, with the global equity index rising 1.0% in sterling terms, supported by strong performance across Asia (shown in yellow) and emerging markets (in red). Improving macroeconomic indicators, easing financial conditions, and resilient earnings sentiment underpinned gains in these regions, offsetting more muted returns across parts of the developed world, particularly the United States.

Within emerging markets, equities across Latin America and Asia rallied sharply, supported by US dollar weakness, favourable duration dynamics, and renewed investor appetite for higher-beta exposures. At a country level, Korea performed especially well, while Brazil also posted notable gains, benefiting from rising commodity prices and improving domestic sentiment. In China, shares in property developers jumped after reports that Beijing had effectively dismantled its long-standing “three red lines” policy, removing borrowing limits that had constrained developers and contributed to a prolonged debt crisis. While largely symbolic and insufficient to resolve deeper structural challenges, the move was interpreted as an acknowledgment that policy tightening had gone too far in a sector central to household wealth and local government finances.

Across developed markets, performance was more mixed. In the US, January marked a continuation of the style rotation that had begun to surface at various points in 2025. Value-oriented and cyclical sectors outperformed growth, signalling a pause in the multi-year dominance of growth and AI-related themes. The region’s technology index, the Nasdaq (above in pink), edged down 0.9%, while the broader S&P 500 (in green) fell 0.5%, lagging both small-cap equities and many international markets. The “Magnificent Seven” underperformed the broader index, highlighting increasing investor sensitivity to valuation, earnings quality, and capital intensity.

This shift was reinforced by heightened earnings-related volatility within the US technology sector. A notable example was Microsoft, which recorded its largest one-day share price decline since March 2020. Despite delivering strong earnings growth, investor concerns around elevated capital expenditure and the lengthening payback period for AI-related investment weighed on sentiment. This episode underscored growing selectivity within what had previously been a broadly supported technology complex, as markets increasingly differentiate between revenue growth, capital efficiency, and long-term returns on investment.

Elsewhere, Japanese equities (above in blue) delivered one of the strongest performances among developed markets, rising 4.5%. Equity strength was underpinned by ongoing corporate governance reforms, robust capital expenditure trends, and improving consumer sentiment. Investor confidence was further boosted by a surprise election announcement from Prime Minister Sanae Takaichi, who is seeking a strengthened mandate for her reflationary policy agenda centred on fiscal stimulus, tax reductions, and wage growth. While equity markets welcomed the growth narrative, bond markets were more cautious, reflecting concerns around increased government borrowing given Japan’s already elevated debt burden.

Across Europe and the UK (above in purple and orange, respectively), equity markets posted modest but consistent gains in January. Inflation continued to ease across both regions, while economic indicators began to show early signs of stabilisation. With the European Central Bank expected to maintain policy rates at current levels in the months ahead, and supportive fiscal developments, most notably Germany’s newly implemented 2025 budget, regional confidence has remained firm. These conditions reinforced the positive momentum seen in European equity markets toward the end of last year, when improved policy clarity and resilient earnings helped lift indices to multi-year highs. UK equities displayed similar resilience, underpinned by moderating inflation, gradual real wage growth, and positive spillover effects from strengthening economic conditions across Europe.

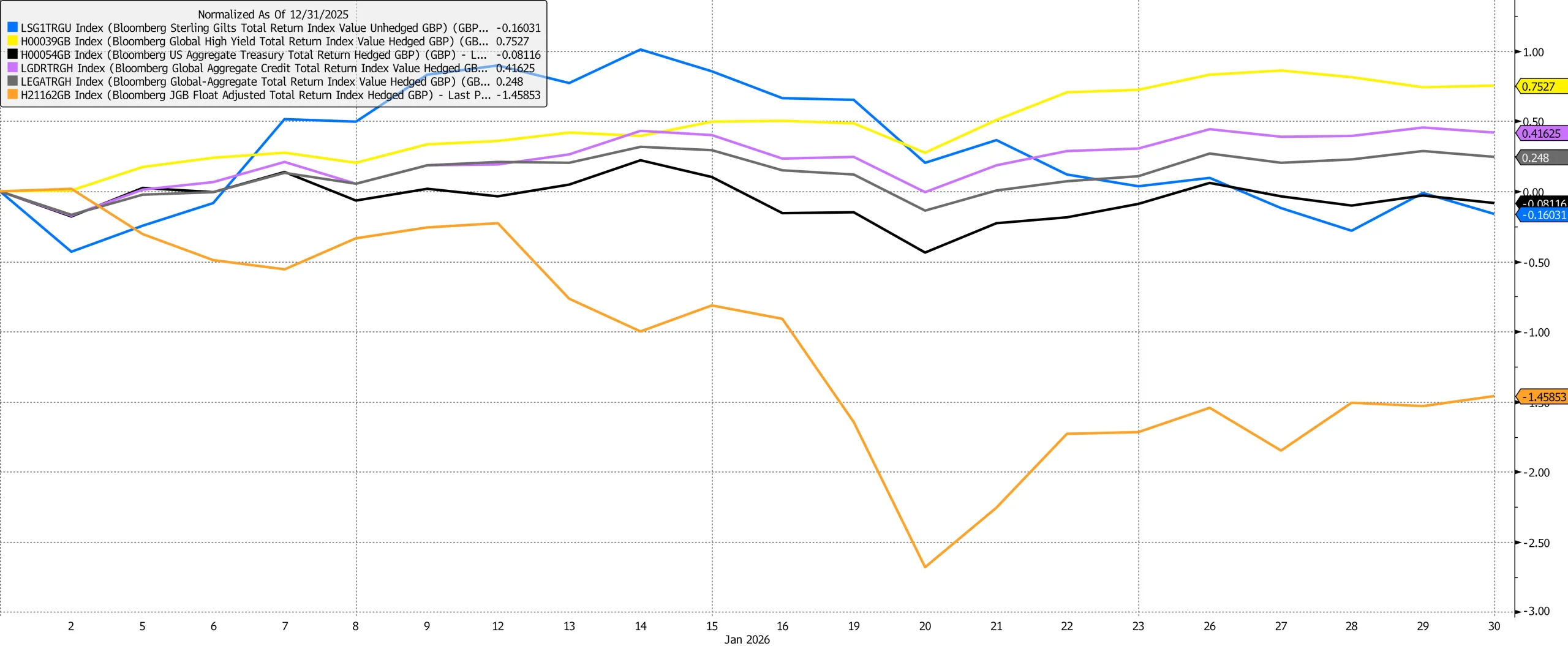

Bond markets added an important additional layer to January’s market narrative. One month into the year, the long end of the government bond curve underperformed across most major markets. Japanese government bonds stood out as the weakest segment, with the yield curve steepening sharply amid rising inflation expectations and concerns over debt sustainability. In contrast, European government bonds outperformed their US and UK counterparts, benefiting from relative policy clarity, easing inflation, and more contained issuance expectations.

Source: Bloomberg

In the US, Treasury markets were more challenging. Although the Federal Reserve held interest rates steady, long-end yields rose through January, leading Treasuries to close the month down 0.1%. The Federal Open Market Committee meeting itself proved largely anticlimactic, with Chair Powell maintaining an optimistic “Goldilocks” tone on the economy, highlighting steady activity and signs of stabilisation in the labour market. Although inflation remains above target, Powell suggested much of the current overshoot is tariff-related and likely to peak in the second quarter of the year.

Corporate credit was a clear winner within fixed income, with the global corporate bond index (in purple, above) rising 0.4% versus 0.2% from the broad global bond index (above in grey). Risk appetite remained firm, global financial conditions continued to loosen, and default expectations stayed contained. Within investment-grade credit, European corporate bonds outperformed, helped by the relative strength of European sovereign markets. Credit spreads tightened modestly, but investors remained selective, favouring balance-sheet strength and regions with supportive policy backdrops.

Commodities also played a meaningful role in shaping market dynamics. Energy prices surprised to the upside, with Brent crude rising by roughly 15% over the, well above consensus expectations for the first quarter of 2026. This move supported energy equities globally and contributed to the outperformance of commodity-linked regions, particularly in emerging markets. The rise in energy prices also fed into bond market dynamics, reinforcing sensitivity at the long end of yield curves.

Looking ahead, we expect markets to remain focused on the trajectory of the US dollar, geopolitical developments, and the evolving global policy landscape. January’s market behaviour points toward a more multipolar investment environment in 2026, where returns are driven less by a single theme or region and more by underlying fundamentals and diversification across geographies, styles, and asset classes.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

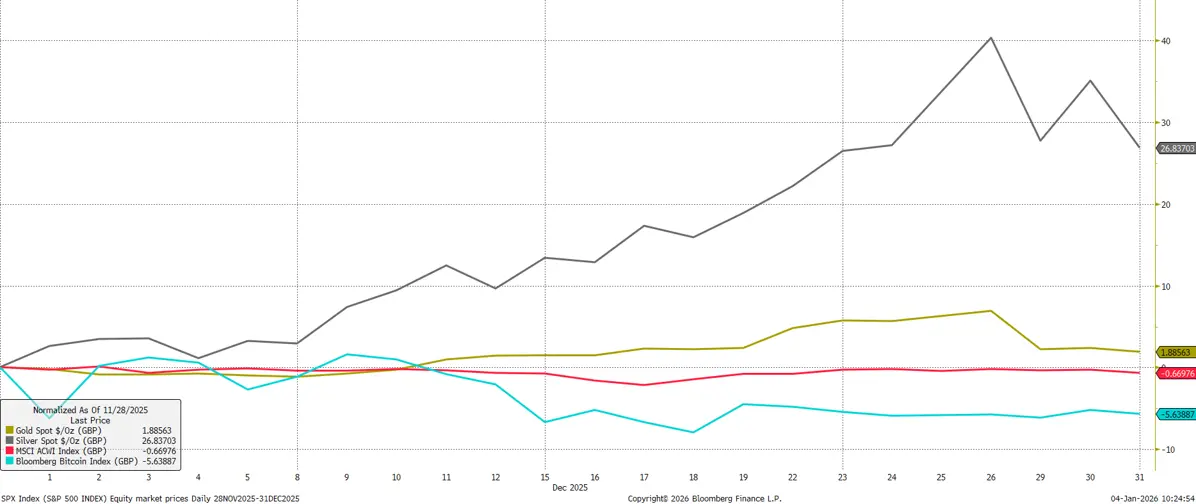

December wrapped up a volatile year with a mix of resilience and rotation.

Outside the US, equity markets finished 2025 on a firmer footing: European and UK equities moved higher in December, helped by their bias toward banks, materials and other “old economy” sectors.

The FTSE 100’s full year story was particularly strong, chalking up its best annual gain since 2009 as investors rewarded cash generative franchises and dividend depth.

By contrast, the US stalled into year end.

In local currency, the S&P 500 was broadly flat for December, but translated returns were softer in sterling as the dollar weakened yet again.

A late month wobble in mega cap technology stocks hurt returns, reminding investors that market leadership can change quickly when valuations are rich and positioning crowded.

![]()

Under the surface, factor signals told a similar tale as in November.

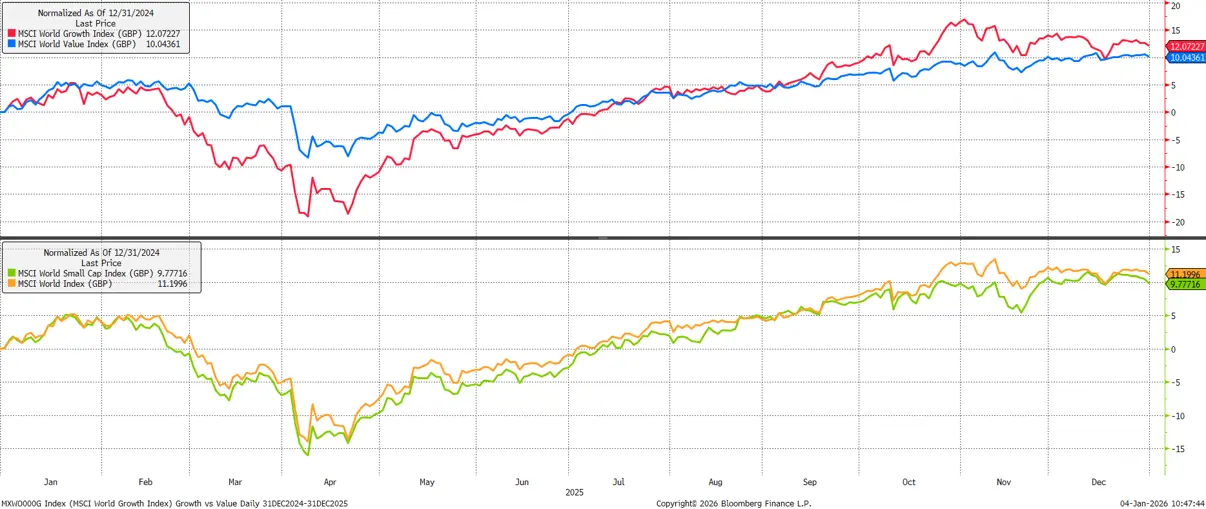

Value stocks outpaced growth counterparts again in December – partly a function of profit taking in the AI complex, partly the straightforward arithmetic of lower multiples.

Small caps were marginally ahead of large caps over the month, but the bigger picture across 2025 was one of convergence: both value and growth ended the year with similar headline returns, even though the value path was less bumpy, proving the importance of diversification:

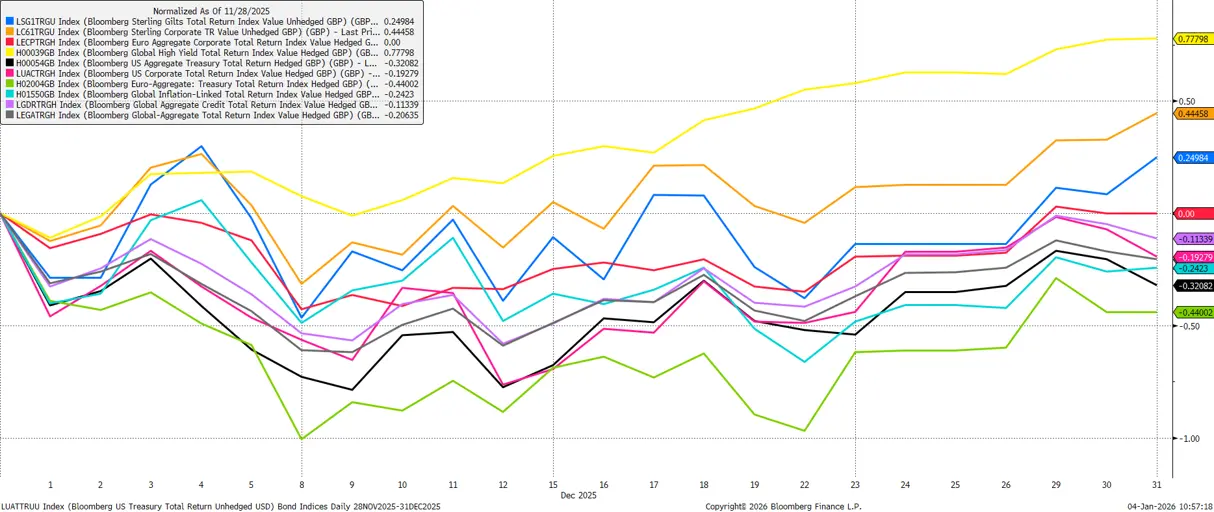

Fixed income had a constructive month particularly in the UK.

Gilts rallied as two things broke in their favour: the Bank of England cut Bank Rate by 0.25% to 3.75%, and November inflation surprised meaningfully to the downside versus consensus expectations.

Neither move was a shock in isolation, but together they sharpened the market’s focus on a gradual, data dependent easing path rather than a race to the bottom.

Credit outperformed government bonds through December, consistent with the late cycle pattern we’ve seen most of the year.

And for 2025 as a whole, bond portfolios did what you’d want in a normalising environment: they earned their keep mostly via income rather than capital appreciation:

Commodities were the standout yet again in December, with precious metals firmly in the spotlight.

Gold made successive record highs and briefly traded above $4,500/oz late in the month; silver’s move was even more dramatic, with a near vertical December that put the closing price around $72/oz and cemented eye catching full year gains of close to 150%.

The drivers are familiar – central bank buying, geopolitical hedging, and, for silver, tight physical markets and strong industrial pull – but the scale of the move forces the risk conversation.

These are useful hedges in the current macro regime, but position sizing needs to respect the higher volatility reality after such outsized returns:

Currencies did their part to shape relative performance.

Sterling strengthened into year end, rising against both the dollar and the yen.

The dollar’s weakness shaved translated US equity returns, with the yen’s slide similarly framing Japan’s softer equity outcome in December.

That yen move was not one way traffic, though, and it arrived alongside an important policy inflection: the Bank of Japan raised its policy rate by 25bp to 0.75%, the highest in three decades.

The message from Tokyo was normalization, not tightness – real rates remain significantly negative – but the signal matters for global asset pricing.

JGB yields edged up, carry strategies re priced at the margin, and investors were reminded that Japan’s regime is moving, even if slowly:

On the policy front elsewhere, December offered clarity with caveats.

The Federal Reserve delivered a third straight 25bp cut, taking the funds rate to 3.50%–3.75% and pairing it with language that was, by design, a shade hawkish.

Minutes made the split obvious: some officials want to guard against an inflation re acceleration, others worry more about a cooling labour market, and both camps prefer to see cleaner data after autumn’s federal government shutdown before committing to a faster path.

In the UK, the BoE’s 5–4 vote to cut underscored a similar balance – disinflation progress is real, but services inflation and the 2026 wage round keep caution front and centre.

The ECB stayed on hold and described policy as “in a good place,” a sensible stance given its updated forecasts and the risk of reading too much into short term resilience.

Inflation prints supported the drift lower without suggesting the job is finished.

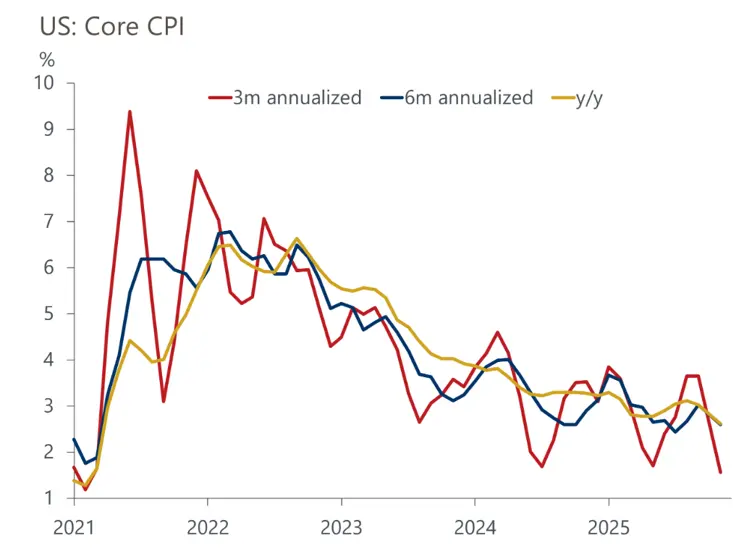

US headline CPI came in at 2.7% year on year with core at 2.6%, the softest pace since 2021; the UK’s November CPI fell to 3.2%, below the Bank’s forecast, with goods disinflation and food prices doing the heavy lifting while services remained stickier.

Both sets of numbers help rate cut narratives, but both are still above target, and both were produced in a year that had sizable data quirks.

The upshot: progress is there; complacency isn’t warranted:

Macro growth data paint a picture of resilience with cooling edges.

The US entered December with robust Q3 GDP and better than expected payrolls, but higher unemployment and a more cautious consumer mix kept markets honest.

Europe’s growth profile remains slower and more uneven, though the equity uplift reflected a different composition story – less exposure to stretched tech, more exposure to sectors that benefit from real assets, capex, and pricing power.

The UK economy remains subdued, but the combination of lower inflation, supportive policy, and equity sector biases was enough to lift domestic benchmarks into year end.

Geopolitics stayed in the background but influenced hedging behaviour.

Energy chokepoints and broader regional tensions didn’t disrupt supply chains meaningfully in December, yet they reinforced the bid for safe haven assets and raised the premium investors place on portfolio insurance.

Policy uncertainty arguably mattered more: the prospect of Fed leadership transition in 2026, the legal trajectory of US trade levies, and the evolving stance on fiscal discipline in several jurisdictions are all live issues for rates, FX and sector dispersion.

The common thread through December is that the macro is getting easier to live with – lower inflation, gentler policy, broader equity participation – but not easy enough to jettison discipline.

Valuations are elevated in pockets, data is still normalizing, and geopolitics can change the narrative quickly.

Portfolios that stayed diversified in 2025 were rewarded. Portfolios that stay selective in 2026 should continue to be.

As we head into 2026, there are reasons for continued optimism: inflation is easing, interest rates should drift down gradually, and growth will likely be positive across regions and sectors, if not stellar.

That mix favours a well diversified portfolio – balancing risk exposures to buffer against any unpleasant surprises that will undoubtedly occur as we move through the year.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

November delivered a two phase adjustment across equities and bonds. The first half was dominated by valuation compression in AI linked equities and uncertainty created by the U.S. data blackout; the second half saw a measured recovery as disinflation signals and the probability of a December policy cut reasserted.

Headline U.S. equities ended the month down around 0.66%, but the composition of returns shifted meaningfully: equal weighted benchmarks and small caps outperformed their market cap weighted peers, value equities exceeded growth counterparts, and sector dispersion widened as leadership narrowed away from the largest technology constituents.

Outside the U.S., developed ex U.S. equities generally provided positive returns, with the exception of Japan, while emerging markets underperformed after a strong year to date run. Asia technology stocks weakened with pressure on high beta names, and China/Taiwan bellwethers reminded investors of the fragility of momentum when positioning is crowded:

Fixed income offered more clarity than equities in November. With the U.S. government effectively reopening on 12 November and alternative inflation indicators signalling ongoing disinflation, the 10‑year Treasury yield drifted toward the 4.0% area into month‑end before firming slightly in early December. This path supported investment grade and high yield bonds in the US and Europe, and while UK bonds were volatile around the budget and the OBR’s accidental leak, prices recovered as investors focused on fiscal‑rule adherence, issuance trajectories and medium‑term discipline; factors that matter to the marginal buyer more than the political theatrics:

Currencies and commodities reinforced the month’s regime. Sterling firmed modestly on improved policy clarity despite tax‑raising measures; the yen weakened further on looser domestic policy settings and renewed geopolitical friction. Precious metals extended their structural leadership. Gold advanced by nearly 6% to close near $4,220/oz, supported by lower real yields, continued central‑bank demand and persistent macro hedging. Silver rose by over 16% to fresh highs around $56–57/oz, underpinned by tight physical markets and industrial demand. The magnitude of precious‑metal gains contrasted with weakness in crypto and high‑momentum technology, offering practical diversification rather than merely theoretical hedging:

Macro policy developments were relevant through their impact on expectations rather than via surprise. In the United States, the 43‑day government shutdown impaired the publication of key data releases, including the cancellation of October CPI, and forced markets to triangulate from private proxies and high‑frequency series. As agencies resumed operations, rate‑cut odds re‑accelerated into month‑end against a backdrop of moderating inflation and softening labour‑market indicators:

In the United Kingdom, announced budget policies were slated to raise roughly £26bn in new tax measures by 2029/30; lifting fiscal headroom to c.£22bn and preserving adherence to the government’s fiscal rules. While productivity downgrades and the back‑loaded nature of the planned fiscal tightening tempered medium‑term growth expectations, the near‑term market reaction centred on sustainability rather than stimulus:

The Bank of England voted 5–4 on 6 November to hold Bank Rate at 4.0%, judging disinflation to be proceeding, and signalled that further reductions would be contingent on continued progress toward the 2% target. The message was gradualism rather than haste. The ECB maintained its meeting‑by‑meeting stance and characterised policy as “in a good place” with inflation near target, reducing the likelihood of policy‑driven surprises in euro‑area assets. Combined, the major central banks’ posture supports a lower‑volatility backdrop for duration and quality credit, with the locus of uncertainty shifting to growth composition rather than inflation trajectory.

As we head into 2026, there are reasons for continued optimism: inflation is easing, interest rates should drift down gradually, and growth will likely be positive across regions and sectors, if not stellar. That mix favours a well‑diversified portfolio—balancing risk exposures to buffer against any unpleasant surprises that will undoubtedly occur as we move through the year.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

October was a month that kept investors on their toes, with plenty of moving parts across asset classes and regions.

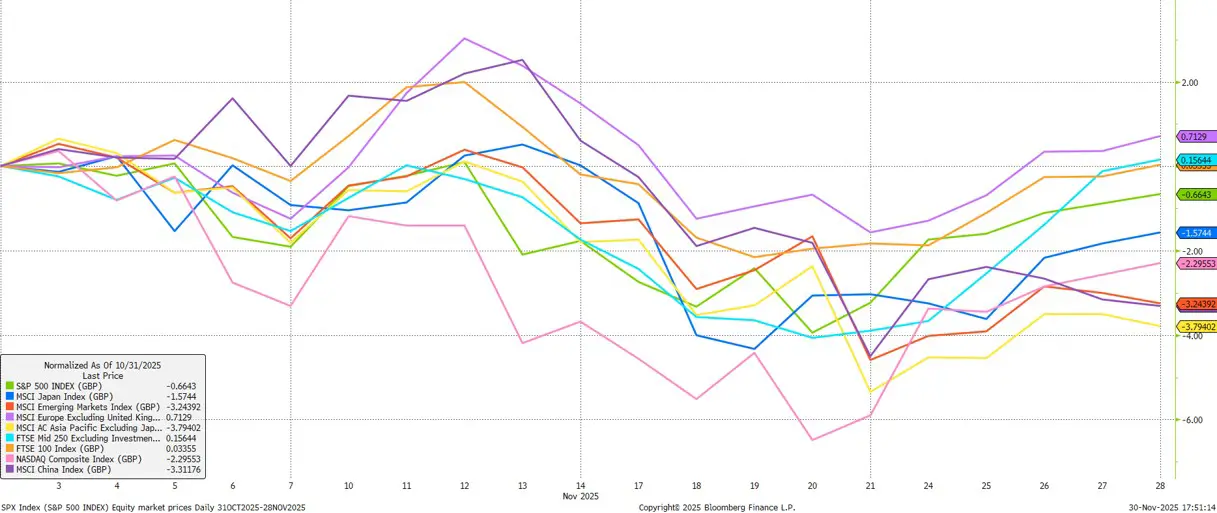

Equities had another strong run, especially in Emerging Markets and Asia ex-Japan which rose by over 6% in both cases. Domestic demand, AI-driven tech momentum, and supportive monetary policy were the main drivers. The US market was led by the “Magnificent Seven” mega-cap tech stocks – illustrated by the strong performance of the NASDAQ index – whose Q3 earnings were robust, particularly in cloud and AI segments. Their performance lifted the S&P 500, even as some of the broader index constituents lagged. The ongoing US government shutdown was a headline risk, but so far hasn’t overly dented market performance.

Chinese equities were notable laggards in October, falling by around 1.5% and taking a bit of a breather from the very strong performance seen in August and September. Still, as mentioned above, broader EM and Asian markets were very strong, with India, Taiwan, and South Korea all posting impressive gains. Japanese equities also posted handsome gains, helped by a weaker yen and a surprise pro-stimulus election result.

UK equities also underperformed, and particularly domestically focused stocks as represented by the FTSE 250 index which rose by just 0.3%. UK macroeconomic data were soft, with GDP and PMI readings disappointing, and inflation remained stubbornly above target. More attention will turn to UK assets next month as the upcoming budget on 26th November is eagerly anticipated.

Bond markets were generally positive as well. Here, UK assets were the standout performers, with UK Gilts rising 2.9% – their best month in nearly two years thanks to softer than expected (though still high) inflation data and expectations for Bank of England rate cuts, and investment grade corporate bonds rising by 2.2%.

At the other end of the spectrum, while still positive, US assets were relatively weak as they gave up some of the previous months’ outperformance. While the Federal Reserve cut interest rates as expected, and announced an end to ‘Quantitative Tightening’, the rhetoric from Jerome Powell was more hawkish than expected on forward looking policy, which disappointed markets somewhat:

On the macroeconomic front, the global backdrop remains supportive for risk assets. US economic data pointed to moderation, with GDP growth slowing but still resilient. Headline inflation ticked up slightly, while core inflation eased marginally, reinforcing expectations for further monetary support. As mentioned, above the Fed’s rate cut was widely anticipated, but Chair Powell’s cautious tone on future policy disappointed some market participants.

In the UK, GDP grew just 0.1% in August after a similar decline in July, while unemployment edged higher and inflation held steady at 3.8%, marginally below forecasts. Subdued growth expectations and positioning ahead of November’s Budget pushed Gilt yields to three-month lows. In Europe, inflation moderated further to 2.1% in October, moving close to the ECB’s target and reinforcing expectations that policymakers will maintain their patient stance.

US fiscal and tariff policies remained central to the macro narrative. While major, market-moving tariff headlines are less frequent than earlier in the year, protracted negotiations most notably with China still have the potential to surprise positively or negatively, and must be closely watched.

The US federal government shutdown began on 1st October, with major services shuttered and workers furloughed. The primary dispute is ostensibly centred around healthcare spending, and while shutdowns aren’t uncommon, at the time of writing this one is notable for now being the longest in history, currently spanning 38 days:

Each week of shutdown is estimated to reduce annualized GDP growth by 0.1–0.2 percentage points, or up to $15bn per week, and the longer the shutdown persists, the greater the risk to government-funded programs and investor sentiment. Markets have largely looked through the headline risk so far as most of the damage caused by the shutdown will be reversed as federal employees receive back pay, delayed federal contracts are finally approved, and social benefits like SNAP resume in full.

However, the lack of government data makes it difficult to determine whether there have been significant spillover effects from the shutdown into the private sector. For example, jobless claims data point to some private-sector layoffs in States most exposed to the shutdown, but the full impact will only be known once the government reopens for business.

Overall, October reinforced the importance of agility and vigilance in portfolio management. While markets have shown resilience, the interplay of monetary policy, fiscal dynamics, and geopolitical risk continues to drive volatility and opportunity. We remain constructive but cautious, favouring quality, diversification, and active risk management as the global landscape evolves.

For a more detailed look at this month’s update, listen to our Market Update podcast. Join Investment Director Oliver Stone and Portfolio Manager Harry Scargill as they break down the key market developments shaping October. From equities and fixed income to macroeconomic trends and the evolving policy landscape, our experts share timely insights to help you navigate the months ahead.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

September saw a continuation of the year’s risk-on momentum, with global equities posting strong gains. The S&P 500 returned 3.7%, marking its best September in 15 years—a notable feat given the month’s historical volatility. The NASDAQ outperformed, up nearly 6%, as US tech stocks benefited from AI-driven optimism and resilient earnings.

China’s equity market led major regions, rising 7.6%, propelled by policy support for domestic chipmakers and a surge in AI investment. The Hang Seng Tech Index gained 22% for the quarter, with Alibaba and TSMC posting outsized monthly gains.

Japan’s Nikkei rose 3.1%, supported by a weaker yen, ongoing corporate reforms, and a surprise prime ministerial election result that markets interpreted as pro-stimulus. The new PM’s victory triggered a sharp rally in equities in early October, though long-dated JGB yields and the yen weakened on renewed fiscal concerns.

UK equities lagged, with the FTSE 100 and 250 up just 1.3–1.4%. Domestic macro data disappointed, with GDP and PMI readings softening, and inflation remaining stubbornly above target. European equities posted modest gains, but French political risk resurfaced, threatening deficit reduction plans and pressuring the bond market:

Precious metals were the standout asset class. Gold surged 11% in GBP terms, trading near $3,900/oz—a new all-time high. Silver rallied 14.6%, approaching its 2011 peak of $50/oz. The rally was driven by a confluence of factors: lower real yields, a weaker US dollar, persistent inflation, and heightened geopolitical risk. Central banks, notably China, continued to accumulate bullion, while private investors poured record inflows into gold-backed ETFs:

The technical picture for gold and silver is stretched, with prices having doubled in less than two years. While the medium-term outlook remains constructive, near-term consolidation is possible given the speed and magnitude of recent gains.

Bond markets stabilised in September, with US Treasuries up 1% as the Fed delivered a dovish rate cut. Investment grade corporate bonds outperformed; particularly those US denominated, benefiting from spread compression, while high yield lagged slightly as spreads widened modestly.

Long-dated government bond yields remained below August highs, but the UK’s 30-year Gilt yield reached 5.6%, its highest since the late 1990s, underscoring persistent worries about fiscal sustainability.

The main macroeconomic headline in September was the Federal Reserve’s pivot to monetary easing; cutting rates by 25bps and signalling scope for further cuts this year. The decision was framed as risk-management, with downside risks to employment outweighing inflation concerns. The ECB and BoE held rates, maintaining a cautious tone and emphasising data dependence. The Bank of Japan stood pat but delivered a hawkish message, only to see expectations upended by the election result.

US fiscal and tariff policies remained central to the macro narrative. The trade-weighted tariff rate now exceeds 18%, reminiscent of 1930s levels, but actual duties paid are still catching up. The growth and price impacts of tariffs are likely to intensify in coming quarters, with baseline US growth expectations remaining resilient for now.

The US federal government shutdown began on October 1, with major services shuttered and workers furloughed. The primary dispute centres on healthcare spending. While shutdowns are not uncommon, the current episode is notable for its potential duration and the administration’s threat of permanent layoffs in federal departments. Per Oxford Economics’ analysis, each week of shutdown is estimated to reduce annualised GDP growth by 0.1–0.2 percentage points, or up to $15bn per week. The longer the shutdown persists, the greater the risk to government-funded programmes and investor sentiment.

Markets have largely looked through the headline risk so far, focusing on the rate path and incoming data, though delays in key economic releases (e.g., jobs and inflation) could increase uncertainty.

The overall environment remains moderately supportive for risk assets, with steady growth, stable (if elevated) inflation, and central banks signalling further easing. However, uncertainty is elevated, and policy decisions will remain data-dependent.

Careful monitoring of economic indicators, policy signals, and geopolitical developments will be essential in the months ahead. While conditions remain broadly constructive, prudent risk management and portfolio diversification are warranted.

Overall, September 2025 reinforced the importance of agility and vigilance in portfolio management. While markets have shown resilience, the interplay of monetary policy, fiscal dynamics, and geopolitical risk continues to drive volatility and opportunity. We remain constructive but cautious, favouring quality, diversification, and active risk management as the global landscape evolves.

For a more detailed look at this month’s update, listen to our Market Update podcast. Join Portfolio Manager Imogen Hambly and Investment Director Oliver Stone as they break down the key market developments shaping September.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

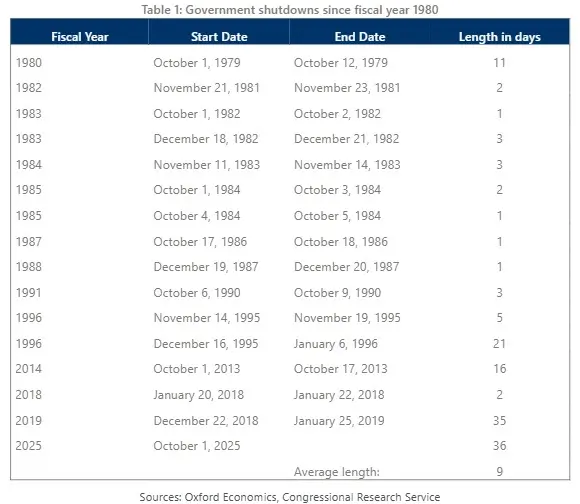

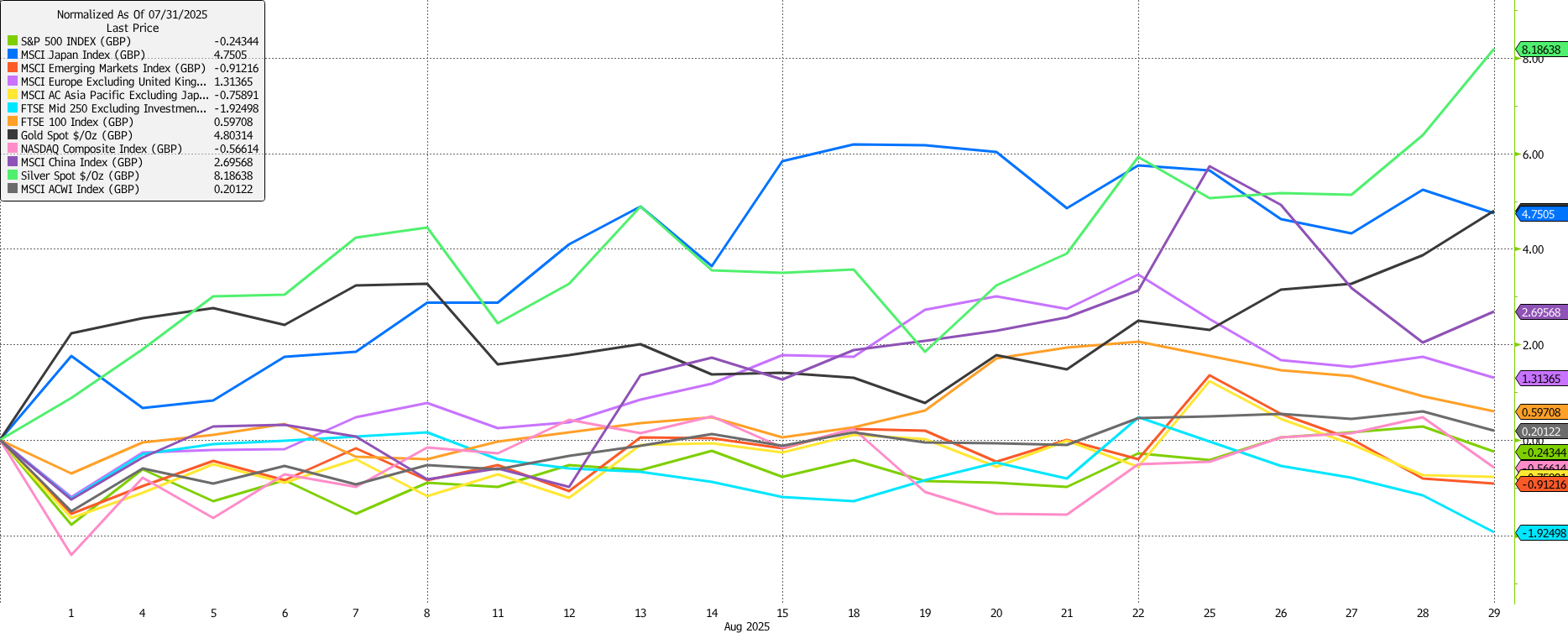

August delivered a mixed but generally resilient performance across global markets. Equities absorbed tariff headlines and political noise to post modest gains overall, though leadership rotated meaningfully. Japan outperformed, rising around 4.8% in GBP terms, supported by a weaker yen and tariff relief for automakers. In contrast, UK equities lagged, with the FTSE 250 down nearly 2% amid domestic policy uncertainty, a surprise inflation uptick, and renewed speculation over potential government revenue-raising measures.

Continental Europe eked out a small gain (1.3%) but lost momentum into month-end as French political risk resurfaced following the Prime Minister’s surprising announcement of a confidence vote on 8th September. Given the administration’s lack of support in parliament, he’s likely to lose the vote which means President Macron will then have three options: call for a new parliamentary election; ask the PM to stay in charge of a caretaker government; or nominate a new prime minister. The last option is probably the most likely and would just about keep the plates spinning, but would likely stymie the deficit reduction plans for 2026 and continue to put pressure on the French bond market.

Precious metals were standout performers this month standout. Gold tested new highs near $3,500/oz, and silver broke $40/oz for the first time since 2012, reflecting a combination of policy uncertainty, softer late-month US dollar tone, and demand for hedges.

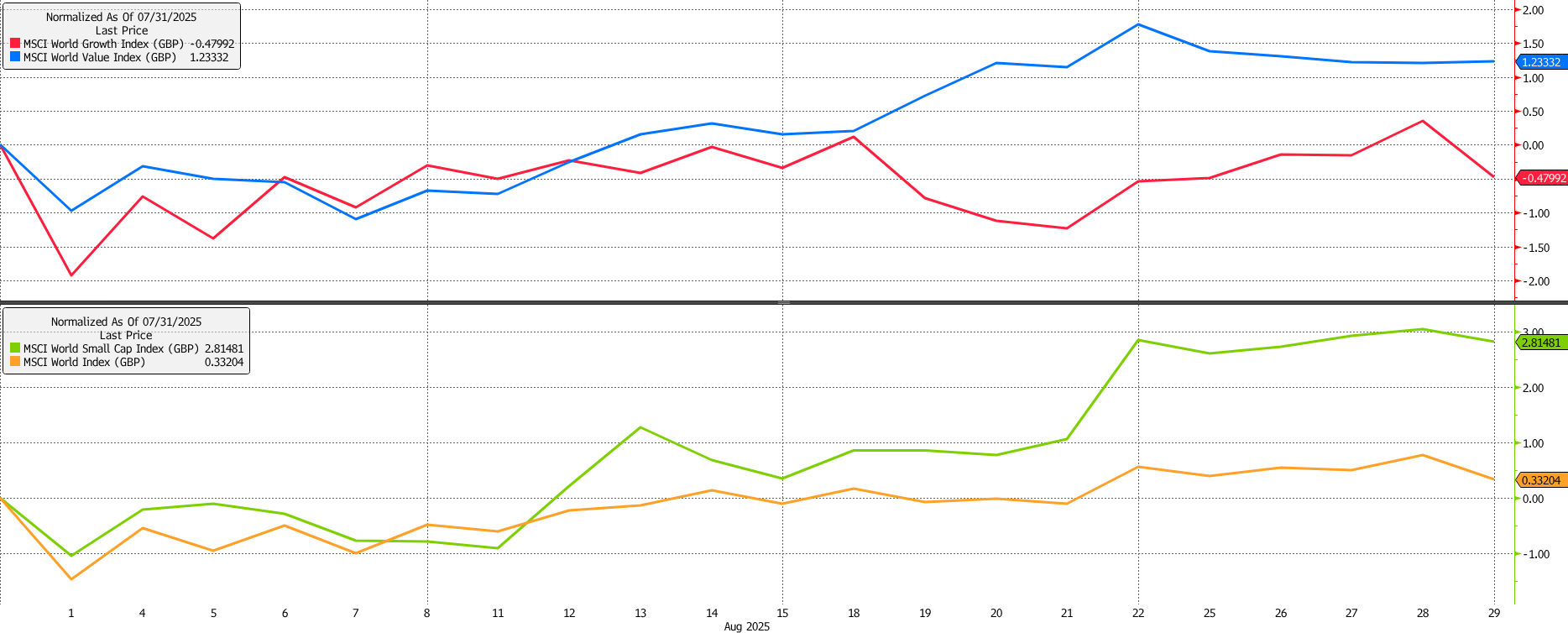

Style and size factors diverged: value outperformed growth, aided by higher long-dated government bond yields and general sector composition, while small caps rallied on expectations of earlier US Federal Reserve easing following Chairman Jerome Powell’s Jackson Hole Symposium remarks. Mega-cap growth names faced idiosyncratic pressure; most notably NVIDIA, where strong absolute results were overshadowed by slowing growth rates and potential tariff-related headwinds.

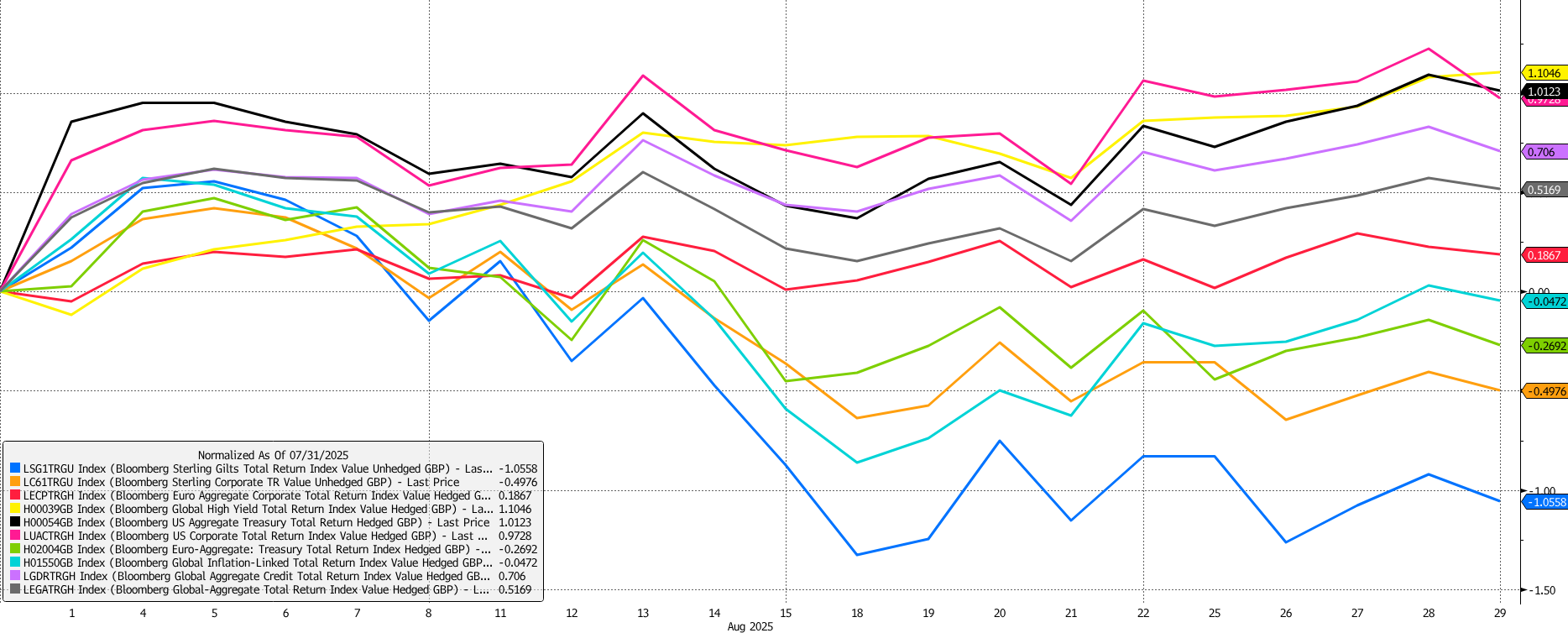

In fixed income, US Treasuries posted positive returns (1%) as yields dropped on dovish Fed signals, while global high yield bonds were once again the best performers, benefitting from their risk-on link to equities and gaining 1.1% on continued spread compression.

Gilts were a notable underperformer, falling by 1.1% as particularly longer maturity yields rose. 30-year Gilt yields reached 5.6%; their highest since the late 1990s.

In the US, as noted above, Jerome Powell’s Jackson Hole speech really moved the dial as he heavily implied that a rate cut is coming in September, while placing more emphasis than before on the relative weakness of the labour market. Meanwhile, the threat of tariffs disruption remains a spectral presence in markets; the announced, trade weighted rate is now north of 18%—a 1930s style headline—but duties actually paid are still catching up. This means that some of the growth and price impacts are likely still ahead, not behind us. Even so, baseline US growth expectations haven’t fallen, which helps explain why risk assets have remained resilient.

We saw a different narrative unfold in the UK. The Bank of England cut interest rates by 0.25% to 4.0%, but the vote passed on a knife edge, and the tone of the Monetary Policy Committee’s comments were hawkish enough to keep a lid on bond market enthusiasm.

The overall environment remains moderately supportive, but uncertainty is elevated. Growth is steady in most regions, inflation is stable if still above targets, and central banks are still on balance signalling a shift toward lower rates. However, policy decisions will remain data‑dependent, and political developments—covering trade policy, fiscal pressures, and governance—could influence market sentiment. We expect conditions to remain broadly constructive, but risks are meaningful; careful monitoring of economic indicators and policy signals will be important in the months ahead.

For a deeper dive into August’s market performance, listen to our Market Update podcast as Portfolio Manager, Harry Scargill, and Investment Director, Oliver Stone, CFA, break down the major movements and developments.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

July was a month of cautious optimism across global financial markets. Risk assets broadly moved higher, central banks struck a more dovish tone, and geopolitical tensions—while still present—showed signs of de-escalation. Yet beneath the surface, the macroeconomic and policy landscape remains complex, with trade dynamics, inflation trajectories, and fiscal pressures continuing to shape investor sentiment.

Global equities delivered strong returns, building on the momentum from Q2. Chinese equities led the way, gaining over 8% in GBP terms and recovering some of the lost ground seen this year after tariff-related relief. The NASDAQ was also strong, up around 7.5% in GBP terms, fuelled by robust earnings from large-cap tech and AI-focused firms. Encouragingly, market breadth improved, with the equal-weighted S&P 500 rising 3.5%, suggesting the rally extended beyond the usual mega-cap suspects.

UK equities also had a good month in absolute terms, with the large-cap FTSE 100 gaining 4.2%, benefitting from its commodity-heavy composition which saw better earnings and a brighter outlook for energy and materials:

Bond markets were more subdued. Early-month weakness gave way to an anaemic rally in the latter two weeks of July, but government bond yields remain stubbornly high, driven by still-robust economic data and increased government debt issuance. For the most part, this left returns broadly flat to modestly negative across fixed income.

In the UK, the 10-year gilt yield edged up from 4.45% to 4.53%, reflecting persistent inflation and fiscal concerns. The Bank of England’s decision to cut rates by 25bps to 4% was narrowly passed, with a second round of voting required. The MPC’s messaging remains mixed, balancing signs of labour market fragility with lingering inflationary pressures. While another cut in November is still expected, confidence in that call has waned.

Across the Atlantic, the Fed held rates steady at 5.25%, but July’s weaker-than-expected jobs report—alongside downward revisions to May and June—has raised the odds of an earlier rate cut. The unemployment rate ticked up to 4.2%, and the foreign-born labour force shrank significantly, reflecting the impact of Trump’s immigration policies:

Inflation data was a mixed bag. In the US, core CPI surprised to the downside, reinforcing disinflationary trends. However, headline inflation remains sticky, particularly in services and food. The UK saw an unexpected rise in headline inflation to 3.6%, the highest since January 2024. Despite this, markets still anticipate further rate cuts, driven by weakening labour market indicators and sluggish growth.

Europe’s inflation hovered around the 2% target, allowing the ECB to pause its easing cycle after eight consecutive cuts. The central bank’s dovish stance has helped anchor rate expectations, though fiscal challenges and trade uncertainty continue to cloud the outlook.

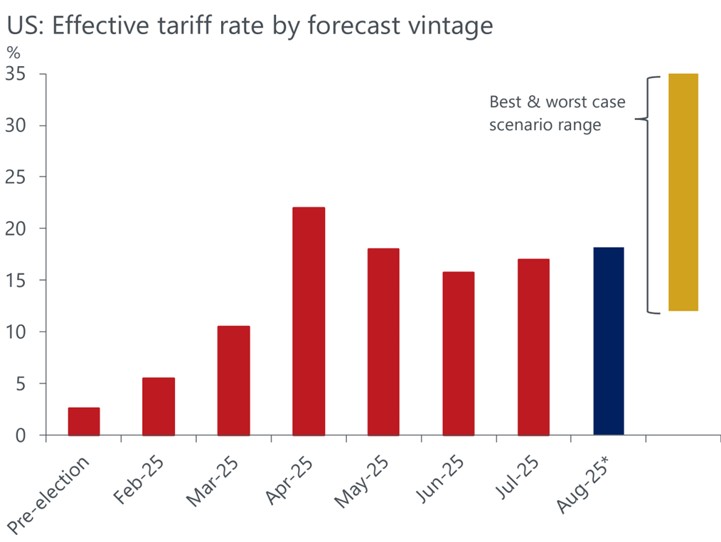

Trade policy remained a dominant theme. The Trump administration’s “One Big Beautiful Bill Act” and a flurry of trade agreements helped calm markets, but effective tariff rates are creeping higher again. As of August 1, the statutory tariff rate stood at 18.2%, up from 17% in July. While headline rates have moderated for many countries, exemptions and preferential deals mean the actual impact varies widely:

For a deeper dive in to the July update, listen to our podcast with Portfolio Manager Harry Scargill and Investment Director Oliver Stone as they break down the key market themes that shaped the month.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

June saw a broadly positive performance across equity markets, with most global indices rising as risk sentiment improved. This came despite escalating geopolitical tensions in the Middle East. US equities in the form of the tech-heavy NASDAQ index were the top performers, rising by 4.6% in pound terms, while the UK was a notable laggard, with the FTSE 100 posting negative returns of -0.13%, reflecting domestic macroeconomic and political concerns.

Silver prices surged nearly 9.5% during the month, beginning to catch up with gold’s performance which has been setting a series of new all-time highs over the past year. This pattern is typical in the early stages of a precious metals bull market and may continue if the trend persists:

This improved sentiment followed the delay in US tariff implementation, with President Trump signaling a willingness to negotiate. This helped reduce perceived recession risks among global corporates, although growth expectations still remain well below levels seen earlier in the year:

Bond markets were volatile. Sterling assets performed well during June as falling gilt yields (and therefore higher prices) reflected weaker macroeconomic data. However, a sharp drop in gilt prices occurred early in July following a session of Prime Minister’s Questions in which the Chancellor’s job security was questioned, serving to highlight the fragility of UK asset prices to political developments.

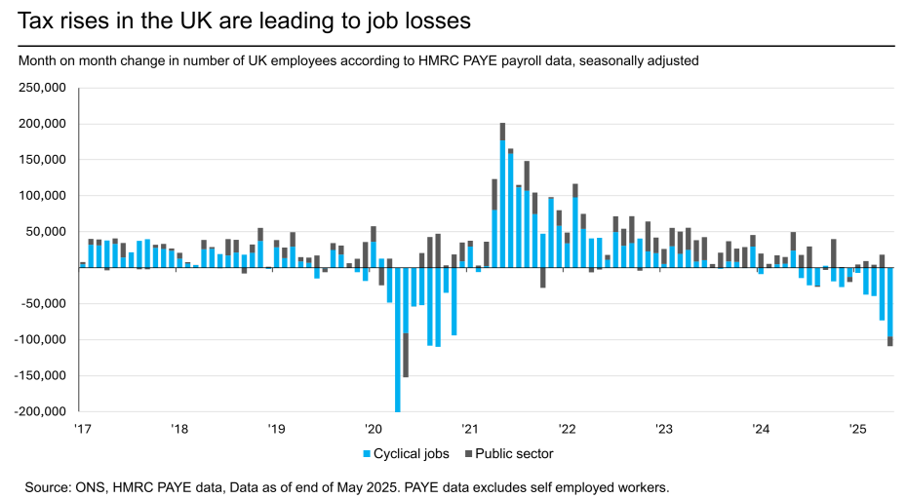

UK jobs data weakened further, with continued losses in cyclical sectors and high candidate availability reported by recruiters. This, combined with fiscal pressures, suggests the UK government may need to tighten policy by £20–30bn in the autumn budget, likely through further tax hikes and threshold freezes.

This places the government in a Catch-22 position; bond markets are expected to react negatively to any perceived fiscal loosening, but equity markets will likely react negatively to further fiscal tightening as animal spirits are crushed:

Geopolitical tensions escalated mid-month with Israel’s Operation Rising Lion and subsequent Iranian retaliation. The US intervened with Operation Midnight Hammer, but a ceasefire was reached within 12 days. Oil and gold prices spiked initially, but markets quickly stabilised, reflecting investor resilience to short-term geopolitical shocks.

Brent crude rose to nearly $80 per barrel during the conflict, driven by fears of supply disruption in the Strait of Hormuz. Although prices eased after the ceasefire, they remain elevated, reflecting a persistent geopolitical risk premium:

The US passed the One Big Beautiful Bill (OBBB), a major tax-and-spending package that will significantly widen the fiscal deficit. The deficit is expected to reach nearly 7% of GDP over the next few years, raising concerns about long-term fiscal sustainability. This has reinforced our preference for shorter-duration bonds:

Tariff policy remains a key macroeconomic variable. The 10% universal tariff and other measures are expected to raise $2.5 trillion in revenue over the next decade. Given the president’s broad authority over trade policy, further changes could occur rapidly and without congressional approval. Retaliatory measures from other countries remain a risk, particularly in the form of non-tariff barriers.

In summary, June was marked by strong equity performance, volatile bond markets, and significant geopolitical and fiscal developments. Diversification remains essential in navigating these complex dynamics and mitigating risks associated with market volatility and economic uncertainty.

For a deeper dive in to the June update, listen to our Market Update podcast where Portfolio Manager Imogen Hambly and Investment Director Oliver Stone unpack the key market events and trends.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.