Market Updates

Harry Scargill

Global equity markets started the year on a positive note, recovering from the headwinds experienced towards the end of 2024. European equities rebounded sharply, posting gains of over 8% in January, following a challenging December driven by concerns around tariffs and weakness in key sectors. The FTSE 100 was another standout performer, rising nearly 6% and reaching an all-time high, marking its best monthly performance since November 2022.

Despite ending well, U.S. equities exhibited significant volatility, particularly in the final week of January, driven by a combination of earnings reports from major technology firms and a significant market shakeup caused by DeepSeek’s Artificial Intelligence (AI) breakthrough. The S&P 500 and Nasdaq saw substantial swings, reflecting the uncertainty around AI-related investments and potential disruptions to the current semiconductor landscape.

Emerging Markets and Asian equities underperformed relative to developed markets, despite exhibiting lower volatility levels. The FTSE 250 also struggled to keep pace with the broader market rally, highlighting continued economic uncertainty in the UK’s mid-cap space.

Bonds had a steadier and more positive month compared to late 2024, with corporate bonds outperforming government bonds. High-yield bonds led the way, reflecting continued investor appetite for risk in a more stable market environment.

Inflation-linked bonds also performed well, supported by concerns over inflation persistence, particularly in the U.S., where upcoming policy decisions and geopolitical risks weighed on sentiment. Market expectations for rate cuts in 2025 have moderated, with fewer cuts now priced in compared to earlier forecasts, leading to upward pressure on bond yields across major developed markets.

Notably, European government bonds were the weakest performer in the bond space, reflecting ongoing economic stagnation and political uncertainty. The European Central Bank (ECB) moved to cut rates to 2.75%, as expected, with markets anticipating similar action from the Bank of England in their February meeting. In contrast, the Federal Reserve opted to hold rates steady, reinforcing expectations of a “higher-for-longer” stance on U.S. interest rates.

The British Pound had a weak month, declining against most major currencies. This was primarily driven by weaker-than-expected economic growth in the UK and a shift in market expectations toward further interest rate cuts by the Bank of England, compared to just a few months ago. Meanwhile, the US dollar strengthened against most currencies, particularly in the latter part of the month, as the implementation of Trump’s proposed trade tariffs began in the final week.

A major event impacting markets in January was the unexpected impact of DeepSeek, a Chinese AI company that launched a highly competitive AI model at, reportedly, a fraction of the cost of its Western counterparts. This triggered widespread concern among investors regarding the sustainability of the heavy capital investments made by major technology firms in AI infrastructure.

The revelation that DeepSeek had trained its model using older and cheaper semiconductor chips sent shockwaves through the semiconductor sector, with Nvidia, in particular, losing nearly $600 billion in market capitalisation in a single session. To put the size of this move into context, only 14 listed companies in the world have a market capitalisation higher than the amount that Nvidia lost.

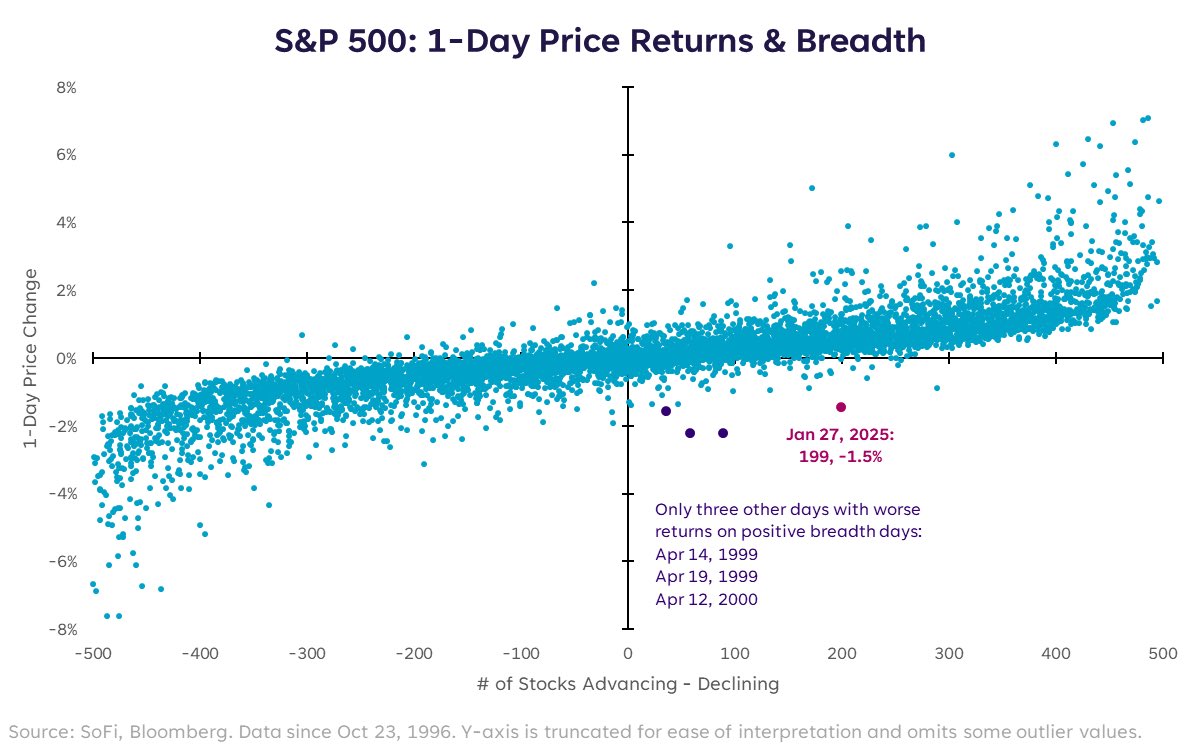

Despite this disruption, broader equity markets demonstrated resilience, with around 300 S&P 500 stocks remaining flat or positive despite the index’s overall decline, as shown in the chart below. This supports the view that equity market leadership is gradually broadening beyond the “Magnificent 7” tech stocks, a trend that may continue through 2025.

January also marked the beginning of President Trump’s second term, bringing with it immediate policy shifts that impacted market sentiment. His administration moved swiftly to implement tariffs, initially suggesting a postponement on Mexico and Canada before abruptly reversing course and imposing 25% tariffs on both nations. Additionally, a 10% tariff was levied on Chinese goods, with the possibility of further increases in the future.

These tariff measures have raised concerns over inflation, as the cost of imported goods will rise and consumers may feel the brunt of these increases. Early estimates suggest that tariffs on Canada and Mexico will have a more significant inflationary impact than those on China, given the changing trade flows since Trump’s first term.

There was, however, a large disparity between those rates cuts that were made and those that had been priced into markets as we came into 2024, which as the year progressed led to elevated levels of market volatility, and in the U.K., caused the Gilt Index to post another year of losses, closing down -3.0%.

Other major bond indices fared slightly better, with falling interest rates and continued economic resilience proving particularly constructive for credit markets, with the Global Aggregate Credit Index eking out an annual return of 3.6%. It was the Global High Yield Index that again gave bond investors the greatest returns though, adding 10.7% and exhibiting low levels of volatility through periods of changing interest rate expectations.

Alongside tariffs, stricter immigration controls were introduced, further tightening an already constrained U.S. labour market. With unemployment at historically low levels, these policies risk exacerbating labour shortages, which could drive wage inflation higher and impact the broader economy. Bond markets have already reacted to these developments, with yields rising in anticipation of prolonged inflationary pressures.

The unpredictability of Trump’s policies, particularly in trade and labour markets, has introduced a new layer of volatility to financial markets. Investors will need to remain adaptable as more clarity emerges on the administration’s long-term economic strategy.

January provided investors with a stark reminder of the importance of diversification and caution in navigating an increasingly complex global economic landscape. While equity markets started the year strong, volatility remains a key theme, particularly in the technology sector.

The bond market’s response to shifting inflation expectations and central bank policy decisions will continue to be a focal point, as investors weigh the impact of higher-for-longer interest rates against slowing global economic growth. Additionally, geopolitical risks, trade policy shifts, and evolving AI investment dynamics will be key factors influencing market direction in the coming months.

As we move further into 2025, maintaining a well-diversified approach and adapting to changing market conditions will be essential for investors seeking to manage risk while capitalising on the available opportunities.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: