Market Updates

Imogen Hambly

Bond and equity markets fell through December, with the MSCI ACWI closing the month down -1.7%, in sterling terms, while the Bloomberg Global Aggregate Bond Index fell -0.9%, driven by an upward repricing of bond yields.

Although December’s Federal Reserve meeting saw Chairman Powell meet market expectations and deliver a 0.25% cut to the US policy rate, the central bank’s supporting narrative shifted, with projections for 2025 moving to reflect just two further cuts through the year, in contrast to the four that were hinted at previously. From a market perspective, this shift towards a higher-for-longer U.S. interest rates scenario puts pay to the perfect backdrop of strong growth plus rate cuts that had been helping support prices through prior months, ultimately leading to losses across both bonds and equities.

From a macroeconomic perspective, however, the U.S. economy remains in good shape. Consumer spending is forecast to be on track for 3% annualised growth in Q4, while healthy consumer balance sheets and strong wage growth continue to provide support. Across the corporate sector, manufacturing activity beat expectations through December, increasing to its highest level since March – a positive sign as we move into the new year.

Elsewhere, Chinese equities offered a ray of holiday cheer to markets, with the MSCI China index closing the month up 2.7%, in GBP. Despite mounting deflationary pressures across the region and ongoing weakness in economic activity, broadening conviction that 2025 will bring interest rate cuts and significant further stimulus helped bolster Chinese equities through the year end.

In local currency terms, Japanese equities also performed well, gaining 2.8%, as policy normalisation and a moderate resurgence of inflation continued to support the region’s growth outlook and boost broad sentiment. However, for U.K. investors, an appreciation of sterling versus the yen weighed heavily on translated returns, with the MSCI Japan index falling -1.3% in GBP.

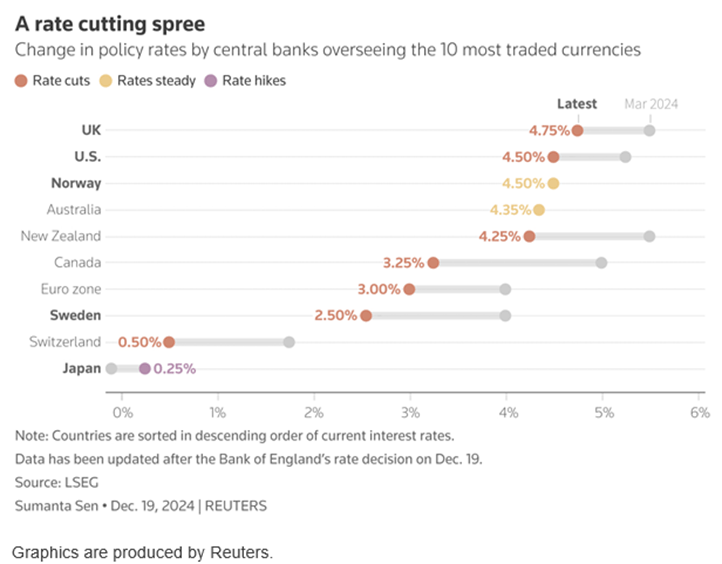

Closer to home, following a 0.3% increase in CPI inflation to 2.6%, the Bank of England (BoE) opted to hold U.K. rates at 4.75% at their December meeting, with officials stating the bank will maintain its “gradual approach” to cuts as we move through 2025 – a move that caused the aforementioned strength in sterling. While the BoE’s action, or lack thereof, was largely priced into markets, it did not stop U.K. government bonds selling off as we progressed through the month, with the U.K. Gilt index ending December down -2.7%.

Losses were also felt across other major global bond indices, with government bonds generally underperforming their corporate counterparts, as changing interest rate expectations pushed up yields. Once again, it was the Global High Yield Index that outperformed, benefitting from an element of spread compression as well as its shorter duration and lower sensitivity to nominal interest rate movements.

Looking back at 2024 as a whole, although markets were disappointed with the level of cuts that were made in some regions, developed market central banks were clear in their intention to begin bringing down policy rates, as illustrated in the chart below.

There was, however, a large disparity between those rates cuts that were made and those that had been priced into markets as we came into 2024, which as the year progressed led to elevated levels of market volatility, and in the U.K., caused the Gilt Index to post another year of losses, closing down -3.0%.

Other major bond indices fared slightly better, with falling interest rates and continued economic resilience proving particularly constructive for credit markets, with the Global Aggregate Credit Index eking out an annual return of 3.6%. It was the Global High Yield Index that again gave bond investors the greatest returns though, adding 10.7% and exhibiting low levels of volatility through periods of changing interest rate expectations.

As we look towards 2025, bond markets undoubtedly offer good opportunity for both growth and income, but we need to look to the year with an element of caution and continue to be selective in where we allocate capital within the fixed income universe. Further cuts to policy rates will certainly help boost returns, however, should economic resilience begin to wane, or inflation surprise to the upside, we will likely see further volatility.

Within equity markets, the picture through 2024 was more positive, driven by exceptional performance from the US ‘Magnificent 7’. From an index perspective, the Nasdaq, shown below in pink, was the standout leader, closing the year up 32.0% in GBP, while the broader US S&P 500 also benefitted from the ramp up in technology valuations, gaining 25%.

While outperformance from US markets has been very well publicised, a number of other good performing areas have flown a little more under the radar. Chinese equities in particular exhibited strength through latter months of 2024, following announcements from Beijing in September that stimulus measures would be put in place to help shore up the region’s ailing property market and get its economy back on track. While equity returns from the region were choppy, low starting valuations and improving investor sentiment allowed the MSCI China Index to gain 18.6%, in GBP.

Japanese equities also performed well, with ongoing corporate reforms helping drive optimism about the economy’s shift towards growth, away from deflation and towards monetary policy normalisation. In March, this saw the Bank of Japan raise interest rates for the first time in 17 years, putting an end to the country’s historic era of negative rates. However, with subsequent hikes bringing the Japanese policy rate to just 0.25%, the yen remains deeply undervalued versus other currencies, a factor that weighed on translated equity returns through the year. In GBP, the MSCI Japan Index, in blue below, returned 9.9%.

Across the U.K., in what was hoped would trigger an economic and market revival, the summer election provided equities with a small mid-year boost of optimism – a feeling that was swiftly reversed following the autumn budget. With higher corporate taxes and higher government spending now expected to put pressure on private sector growth and create stickier inflation, the trajectory of U.K. interest rates is less clear. Come year end, this lack of clarity contributed to the FTSE 100 returning a modest 5.8%.

European equities fared no better, as growth across the region continued to slow, while political issues mounted. German manufacturing activity, which was once the powerhouse of European growth, still sits deep within contractionary territory – under pressure from high energy costs, mounting levels of regulation and growing overseas competition. While political resolution, more stable inflation and falling interest rates should help revive the European economy as we move through 2025, it remains difficult to see any clear drivers of growth.

As we move through the new year, we see reason for optimism, as global economies begin to absorb lower interest rates. Research indicates that corporate earnings are expected to pick up across developed markets, driving GDP growth. Furthermore, where 2024 saw returns concentrated within a small subset of mega cap U.S. technology stocks, it is thought 2025 will bring a broadening in equity market returns, both within the U.S. and globally, with investors much for focused on underlying earnings growth.

But, while the overall picture speaks to positivity, markets have a tendency to surprise, and with a new president about to enter the White House, both the U.S. and wider global economy face a lot of uncertainties.

2024 once again showed us that diversification across portfolios does benefit. There is no question that U.S. technology was exceptional through the year, however it was not the only area to have surprised to the upside. Diversified investors will have seen allocations to China and Japan both add notable levels of value, while fixed income and alternative assets – global high yield, global credit and gold – also benefitted.

Looking forward, retaining this level of diversification will be key to navigating the changing economic and political backdrop, while the ability to adapt will ensure opportunities are taken, if and when they arise.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Our advisers |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: