Market Updates

Oliver Stone

")

After musing last month as to whether July’s positivity was a ‘relief bounce’ rather than the beginning of a sustained recovery, August’s price action provided little evidence to confirm the latter at the expense of the former.

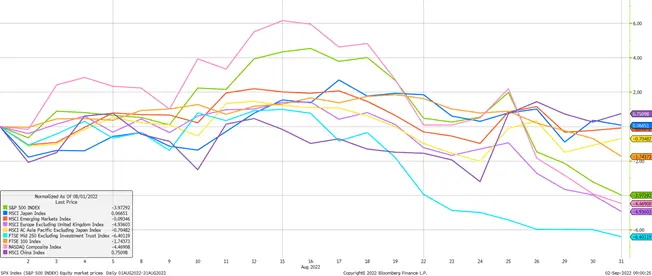

Equity markets held steady for the first half of the month before beginning to roll over as the first chart shows below in local currency terms. Continuing the back-and-forth theme of this year, Asian and emerging market equities were once again the relative winners versus developed market equities. The MSCI China index rose by 0.75%, dragging the broad emerging markets and Asian indices with it, though both recorded small losses.

Japan was by far the best of the developed markets, eking out a 0.07% gain, while US and European indices were further behind, falling by 3.97%-4.93%. The UK saw its large-cap FTSE 100 index performing relatively well, while its mid-cap, domestically focused FTSE 250 more losses, reversing its more positive July in dropping by 6.40%:

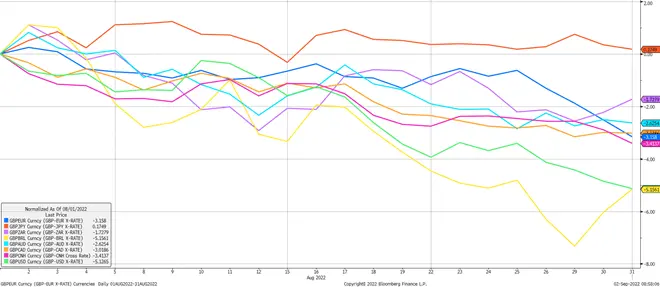

However, for UK investors, this chart doesn’t tell the full story. Again continuing one of 2022’s themes, the second chart below shows that the pound fell precipitously versus all major currencies bar the Japanese yen during August; including by more than 5% against the US dollar:

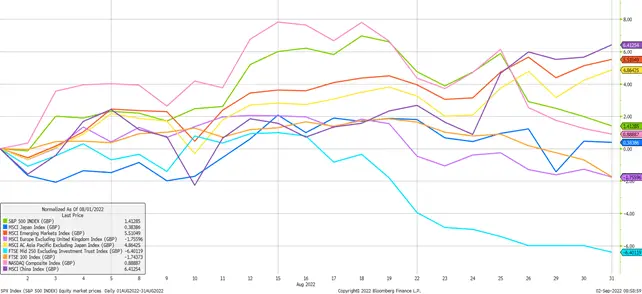

This meant that when equity returns were translated from local currency back into pounds, the results were markedly different as the third chart shows. Returns almost across the board were positive, with only the UK and European indices still languishing in negative territory.

The pound’s weakness came even as the Bank of England’s (BoE) Monetary Policy Committee (MPC) raised interest rates again by 0.5% in their ongoing attempt to bring inflation under control. In theory, this action should have provided some support for the pound, however in making their rate hike decision the BoE made a number of additional pronouncements that undermined this support, expressing worries over the potential for entrenched high inflation, forecasting a recession in 2023, and announcing a reversal of its quantitative easing programme from September onwards.

The bank has been unusually and not always helpfully forthright in its communications this year, with other major central banks striking more nuanced tones.

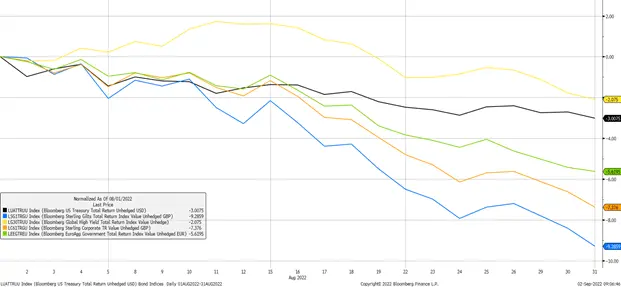

Bond markets suffered another tumultuous month as central banks remained resolutely hawkish; indicating their willingness to risk damaging economies to bring down inflation. Towards the end of the month, the US Federal Reserve Chair Jerome Powell made his eagerly anticipated annual speech at the Jackson Hole Economic Symposium in Wyoming, where he unambiguously stressed the importance of inflation control, and stated that he was prepared to use the central bank’s toolkit ‘forcefully’.

These comments impacted equity markets as seen above but also bond prices as can be seen below. In both cases, investors had been cautiously pricing in the start of a central bank ‘pivot’ away from its current trajectory – a notion that was firmly put aside by Powell. Government bonds were particularly badly affected, with UK Gilts falling by more than 9% during August, European government bonds by 7.38% and US Treasuries by 3.00%. All eyes will now be on monthly inflation data as to central banks’ next moves:

Building on the points we made in last month’s note, as we move into the autumn and winter months, we would caution on the outlook for risk assets should the economic situation deteriorate further from here, despite equity market valuations already looking attractive. Without substantial government intervention consumers and businesses will face a squeeze on incomes and margins due to high inflation; particularly with regards energy prices in the UK and Europe.

Consumers will need to make hard spending choices, with signs that personal debt is already increasing in response to price rises, while businesses will be forced to internalise additional costs themselves or try to pass them on to consumers, resulting in an unpleasant negative feedback loop.

Of course, nothing is certain, and there are many distinct possible pathways from here through to 2023 and beyond. From this month, the UK has a new Prime Minister who has a singular opportunity to enact radical supply side reforms which could be the catalyst to recovery – we hope to be pleasantly surprised.

In light of these risks, as always we would encourage diversification across portfolios, particularly as we look ahead towards the colder months.

We have over 650 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact:

(1)")