Market Updates

Harry Scargill

Starting with bond markets, we saw negative returns for all the major bond indices across April. Largely this negative performance was driven inflation by data which came out during the month, particularly relating to the US and the UK, and which was a little higher than expected. This led investors to push back expectations relating to rate cuts made by the Federal Reserve and the Bank of England. In the US, we saw the March Consumer Price Index (CPI), a key measure of inflation, come in at 3.5%, which was higher than the 3.4% expected. This was the third higher than expected CPI report in a row for the US, and showed that inflation across the pond is remaining stickier than many had expected; particularly services related data which is being supported by a very strong labour market.

European bond markets performed better on a relative basis during April, as their inflation data came in as expected. European CPI for March was 2.4%, which was the same as the February meeting and keeps them quite close to the target level of 2%. The economic backdrop for Europe is also much weaker than we are seeing in the US, and while we are seeing improvements, the market is currently pricing in around a 70% chance that the European Central Bank cuts interest rates in June.

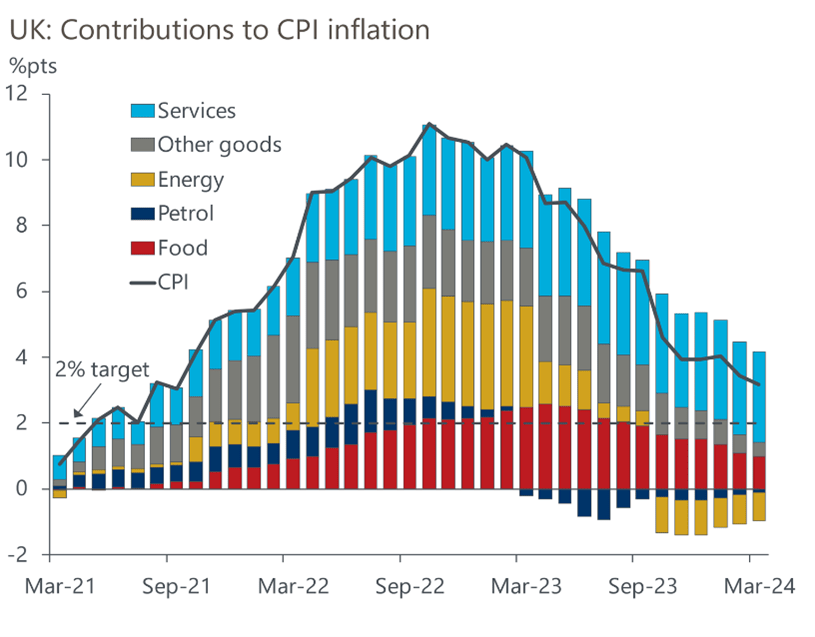

Closer to home, we saw CPI for the UK fall to 3.2% for March, falling from the 3.4% we saw in February and continuing a nice downward trend, as you can see from the chart below. However, the market was disappointed as, like the US, this did not fall by as much as was expected. The key issue being that services related inflation, the blue bar in the chart below, was remaining quite sticky, and that this is the hardest part of inflation for the central banks to influence.

Source: Oxford Economics

The US economic data points towards the potential of interest rates staying higher for longer. Particularly given the strong economic backdrop and the potential risk of inflation increasing at a higher rate were we to see interest rates lowered. In the UK, the weaker economic backdrop arguably means that rates could be lowered from the current level to support growth, while not causing inflation to increase. Despite the higher than expected reading for March, investors are still hopeful for a rate cut by the Bank of England coming within the next couple of meetings.

The change in expectations relating to interest rates was also one of the key drivers of the equity market during the period. April ended as the first month of negative returns for the US equity market, as measured by the S&P500, since October of last year. Given the very high weighting that US equities have in the global index, this dragged down the MSCI World, which finished down 2.9% in GBP.

The worst performing of those shown in the above graph (all returns shown in GBP) was the MSCI Japan index, which fell 3.6%, having been a very strong performing market over the past 12 or so months. However, this was largely driven by further weakness seen in the Japanese Yen, as the market was only down 0.6% in Yen terms. Given the low interest rates in Japan, the likelihood of rates staying higher for longer in markets such as the US and the UK is weighing significantly on their currency’s exchange rate. So much so that during April we saw a joint statement by US Treasury Secretary, Janet Yellen, along with her Japanese and Korean counterparts acknowledging serious concerns relating to sharp depreciation of their currencies. This lends investors to think that the Bank of Japan (BoJ) will step in to intervene with the currency, and that this is supported by the US. This has temporarily supported the Yen, but concerns remain about how much further the BoJ is willing to go to support their currency, or raise interest rates, or even whether they have the ability to do so.

As we already mentioned, US equities were weak during April, with the broader S&P500 losing 3.3%, which was marginally better than the 3.6% loss for the technology heavy NASDAQ. Unlike Japan, this was not due to currency volatility, as local returns, in USD, were weaker than those shown above in GBP. The weakness in the US market was driven by the higher for longer narrative around interest rates, which suggests that the Federal Reserve have a trickier job than other central banks. This also impacted the US more than other markets due to the higher valuation that the US market carries, particularly give the strong performance we have seen from US equities over the last 18 or so months. US earning season for Q1 2024 has also been in full flow, with the majority of the market reporting during April. This was a relatively uneventful earnings season, with the majority of companies performing in-line with expectations. It is clear to see though that the market is laser focussed on future guidance, with this being the more dominant driver of share prices following earnings announcements.

On the positive side of things, we saw Chinese equities as the best performer this month, gaining 7.6% and helping lift broader Asia Ex-Japan and Emerging Market indices. The FTSE100 also performed well, gaining 2.4%, which pushed it through the 8,000 level to hit all time highs. Patience of those invested in the UK therefore beginning to be rewarded, while valuations for the UK market still looking attractive. The FTSE was helped by strong performance in commodity related equities, particularly the miners, which have seen quite significant price increases of the underlying commodities they are associated with. This positive sentiment was given a further boost when BHP Billiton, the once UK listed miner who now trades on the Australian Stock exchange, bid for the UK listed Anglo American. The first offer was for $39bn, which was rejected by Anglo American, and investors are now weighing up whether increased bids are likely to follow, or who else might be targeted.

We discussed precious metals in detail last month, but April was another good period for both silver and gold spot prices. Both of these are also included in the chart above, with gains of 2.5% and 5.3% to gold and silver respectively. Both metals were on for a much stronger gain before they pulled back a little over the last 10 or so days of the month. This pull back was likely driven in part by the changing in rate expectations that we have already discussed.

To conclude, we feel that April has shown that we are still seeing many economies see inflation at higher levels than we thought it might be at the start of the year. This is causing volatility in expectations around interest rates, when they may be cut, and how many rate cuts we can expect in the next 12 months. This is causing ripple effects across major equity and bond markets. We therefore continue to believe this highlights the importance of diversification, particularly given the ongoing geopolitical uncertainty and all the elections that we have this year.

We have over 1000 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: