Market Updates

Oliver Stone

October was a month marked by a series of dynamic and complex developments across global financial markets, with a mix of economic data surprises and political uncertainty creating a multifaceted narrative.

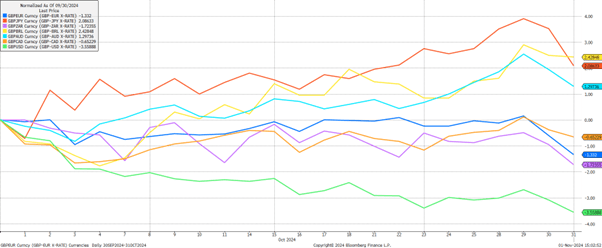

In local currency terms (i.e. unadjusted for GBP fluctuations), equities performed poorly to a greater or lesser extent, with only Japan being positive. However, over the month, GBP was weaker against most major currencies, meaning when translated back to pounds, equity returns were improved, if still lacklustre:

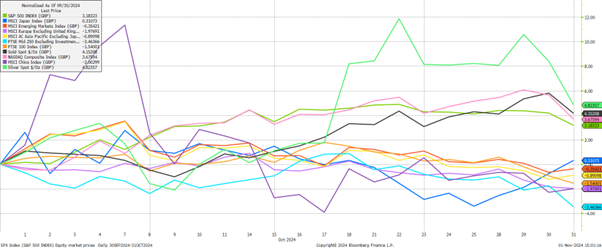

In GBP terms, US equities delivered strong gains as the US dollar rose in value by more than 3.5% against the pound per the chart above (green line above). Underneath the surface, the US index struggled somewhat into the end of the month as big tech earnings disappointed investors; while the absolute quantum of these earnings was, as usual, very impressive, the valuation levels ascribed to them is already very high, meaning investors expect spectacular numbers very quarter, and tend to be disappointed if this is not the case:

Elsewhere, Chinese equity market (purple line above) sentiment was extremely volatile, driven by a cocktail of regulatory concerns and mixed economic data. After a very strong September and start to October, investors grappled with uncertainty as government officials failed to provide further updates around stimulus measures. Further announcements are expected in this month (November), with officials waiting for the US election result before moving forward.

The precious metals market offered some relief, as gold and silver remained in demand (bright green and black lines above). These assets continued to attract investors seeking a hedge against geopolitical, monetary and fiscal policy risks, highlighting the ongoing appeal of real assets, not just as a store of value but also as an opportunity for enhanced returns.

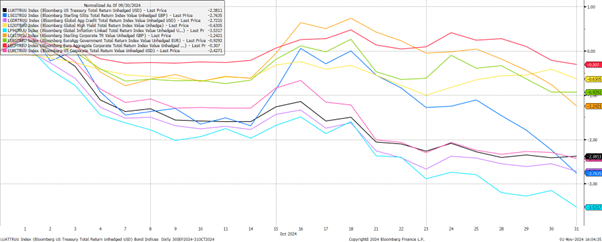

The bond market, meanwhile, presented one of the more puzzling stories of the month. Despite global central banks starting their rate cutting cycles, bond yields have risen over the last month. This unexpected movement reflected broader concerns about fiscal stability, and continued doubts about central banks’ effectiveness in taming inflation The situation was particularly pronounced in the UK, where the highly anticipated budget announcement at the end of the month led to a sharp spike in gilt yields and capital losses in the bond market (dark blue line below):

The government’s new fiscal measures, which included raising the employer National Insurance rate to 15%, adjustments to Capital Gains and Inheritance Tax, and substantial spending increases, were met with scepticism. Investors worried about the government’s ability to manage economic challenges while pursuing such expansive spending policies, resulting in the Gilt yield spike above, a weaker pound and weaker domestic equities.

The Office for Budget Responsibility (OBR) offered a grim analysis of the budget. Their assessment painted a picture of lower GDP growth, reduced labour market participation and disposable incomes, and higher inflation, which, in turn, was expected to keep bond yields and interest rates elevated. The coming weeks and months will be crucial for the government to frame their policy suite in a more positive light.

Adding to the global geopolitical complexity was the heightened focus on the upcoming US election. With polls indicating a tight race, the market is braced for various potential outcomes, each carrying significant implications. Regardless of the outcome, both political camps are expected to maintain high levels of fiscal spending, which only adds to the medium-term economic uncertainty in the United States. Volatility remained elevated over the month with every headline pored over in a frenzy by investors; we shall comment on the outcome in next month’s update.

We have over 1250 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: