Market Updates

Imogen Hambly

Despite the volatile start to the month, in the round, August turned out to be a relatively positive period for global markets.

As noted in last month’s summary, the first week of August was dominated by very aggressive moves in the Japanese Yen and the wider Japanese equity market – moves that were driven by a combination of diverging factors.

On one hand, coming into August a number of disappointing US data releases pointed to slowing manufacturing output and a weaker than expected labour market, sparking concerns that the world’s largest economy might be headed towards a recession. This led to a swift change in US interest rate expectations, with investors moving to price in a series of aggressive rate cuts by the US Federal Reserve.

Concurrently, in a bid to control rising Japanese inflation, the Bank of Japan unexpectedly increased interest rates, causing a spike in the value of the Yen – per the chart below, with JPY in red – and forcing an unwind of the so called ‘carry trade’.

As outlined previously, a carry trade is very simply being ‘short’ a low yielding asset and being ‘long’ a higher yielding asset. Another way to think about it is borrowing at a low rate to invest at a higher rate elsewhere.

Unfortunately, those expectations of aggressive interest rate cuts from the US Federal Reserve, coupled with the unforeseen interest rate hike from the Band of Japan meant the differential between the low yielding Japanese Yen and the high yielding US Dollar swiftly contracted, pushing the value of the Yen higher and forcing investors to quickly sell assets to cover currency losses.

Elevated levels of selling across the major equity indices then led to falling prices, with the MSCI Japan index dropping over 20%, in local currency terms, through the first three trading days of August. The US technology index, the Nasdaq, fell over 7% in dollar terms, over the same period.

The technical nature of the correction meant the sell-off was short lived and markets soon began to pick up, buoyed by the prospect of falling interest rates and good Q2 corporate earnings. Come month end, in sterling terms, global equities had reversed all previous losses, closing up 0.2%. On a regional basis, European equities (in purple, above) also performed well, gaining 1.8%, while the FTSE 100 (in orange) added 0.1%.

At the other end of the scale, UK mid-caps (above in light blue) closed down 2.1%, while the Nasdaq (in pink) fell 1.5%, weighed on by a weakening dollar.

Across bond markets, the picture was brighter. Early month volatility saw yields fall and a flight to quality, as weakening US economic data prints and softening inflation figures paved the way for Federal Reserve interest rate cuts. US treasury prices, shown below in black, spiked initially, but later moderated versus other areas of the fixed income space to end the period up 1.3%, ahead of other developed market sovereign bonds.

Credit markets were buoyed by solid corporate earnings and falling sovereign bond yields, with corporate bonds ultimately outperforming government bonds across each of the major regions. The global high yield index was a little more subdued than its investment grade counterpart, with high yield spreads remaining a touch wider, reflecting the added risk associated with slowing growth.

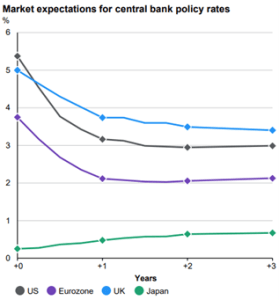

Elsewhere, despite a mid-month bounce, UK government bonds, in dark blue above, closed the month with a modest gain of 0.5%. Across the UK, data prints continue to point to ongoing economic resilience, with manufacturing activity improving and inflation on a clear downward path. However, accelerating activity levels, rising public sector spending and the recently announced energy price cap increase each pose a risk to this otherwise positive inflation picture – leading to expectations that interest rate cuts by the Bank of England may be more gradual versus those of the US Federal Reserve and the European Central Bank, as the below chart indicates.

In contrast, across the US, interest rate cuts are expected to be far more expeditious, with markets currently pricing a 200bp reduction over the next 12 months, as questions over the strength of the labour market fuel recessionary concerns in the region. A weak July unemployment report showed a sharp uptick in initial jobless claims, while the month’s employment data showed a particularly low payrolls increase. However, since the release of these figures, deeper analysis indicates that the level of weakness was largely due to weather and other seasonal factors, while nowcasts indicate the August data are stabilising at slightly more healthy levels.

Despite the encouraging signs, moving into September, US jobs reports are expected to be at the forefront of investors’ minds, with further volatility likely if data disappoints. What’s more, the significance of these data points is not being overlooked by officials, with Federal Reserve Chairman Jay Powell seeking to instil confidence in the markets within his recent speech at the Jackson Hole Annual Economics Symposium, by stating that it is time for the Fed to shift its focus from fighting inflation to maintaining a strong labour market.

This rhetoric is a clear indication that the US central bank is not willing to stand by and observe a further deterioration in employment, and acts as a strong signal to markets that a September US interest rate cut is coming.

Notwithstanding the month’s shaky start, August turned out to be a positive period for balanced investors, with fixed income providing a good element of support to portfolios, particularly through the first few days of the month as equity volatility spiked upwards.

Moving forward, there are undoubtedly questions around the strength of global growth, and more specifically, the strength of US growth. However, while earnings reports remain robust, we are able to focus our attention on valuations, with a broad universe of well-priced and high-quality companies on offer across markets.

We have over 1000 local advisers & staff specialising in investment advice all the way through to retirement planning. Provide some basic details through our quick and easy to use online tool, and we’ll provide you with the perfect match.

Alternatively, sign up to our newsletter to stay up to date with our latest news and expert insights.

| Match me to an adviser | Subscribe to receive updates |

The value of investments may fluctuate in price or value and you may get back less than the amount originally invested. Past performance is not a guide to the future. The views expressed in this publication represent those of the author and do not constitute financial advice.

For further information, please contact:

For further information, please contact: